Rates Unchanged, but the Meaning of "Unchanged" Has Changed

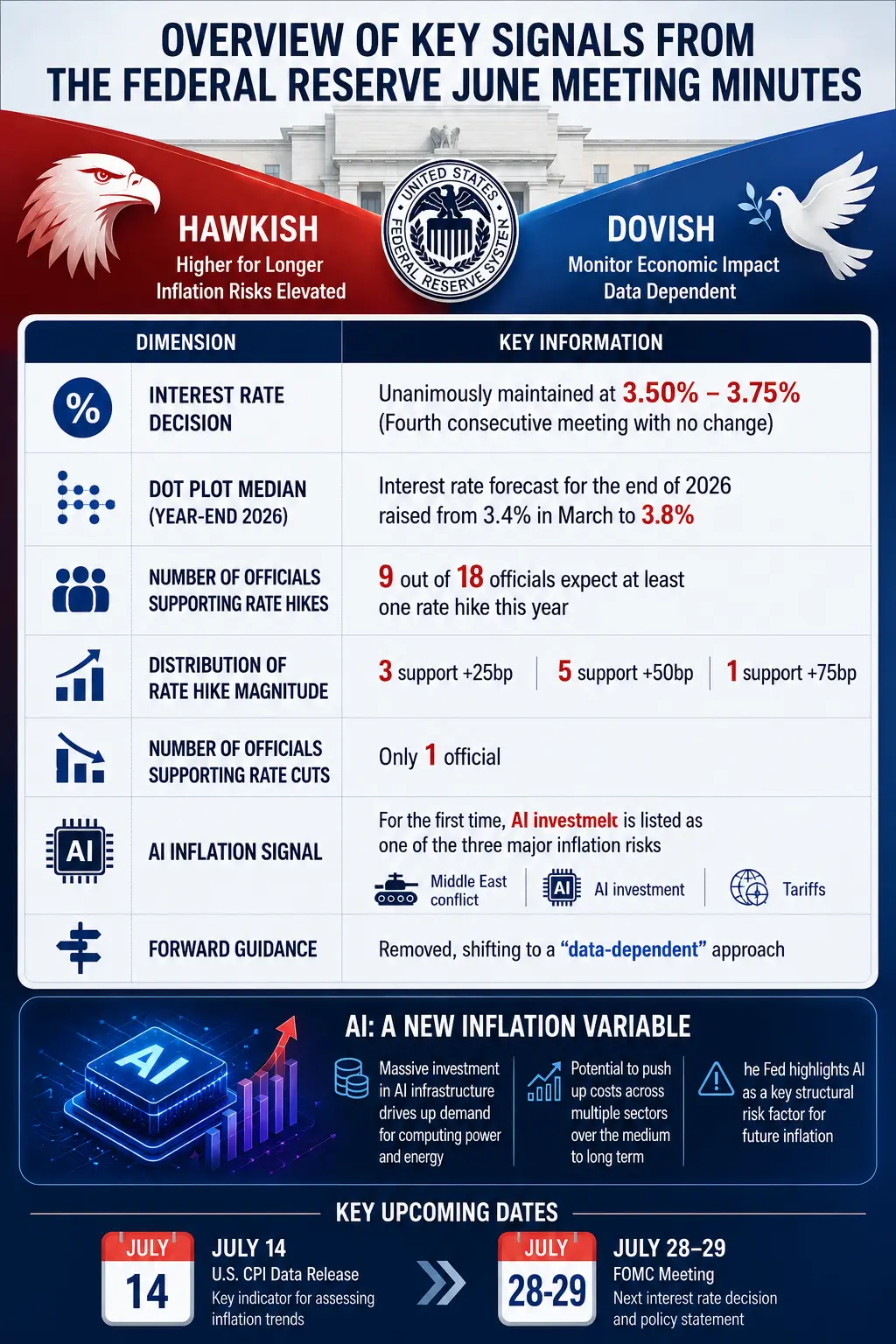

On the surface, the June FOMC meeting results were unsurprising—12 voting members unanimously agreed to keep rates steady. Since December last year, the federal funds rate has remained in the 3.50% to 3.75% range. However, the real focus of this meeting was not the decision itself but the officials’ judgments about the future.

The minutes show that in the economic projections released after the meeting, among 18 participants, 9 believe at least one rate hike is needed before the end of 2026, with 6 expecting two hikes. In March this year, no one held the same view. Meanwhile, the number expecting rate cuts dropped from 12 in March to just 1. The median forecast for the federal funds rate at the end of 2026 was raised from 3.4% in March to 3.8%—implying market expectations of at least one rate hike this year.

But divisions are far from over. Another 9 officials expect rates to stay unchanged or to be cut. The minutes explicitly state that participants’ individual assessments of appropriate monetary policy under their most likely economic scenarios show a “roughly equal” split. Some members believe inflation will gradually cool, providing room for rate cuts; others think prices will remain high, requiring further hikes.

This split is not surprising. U.S. inflation has risen to 4.1% year-over-year, well above the Fed’s 2% target, with prices exceeding the target range for six consecutive years. In May, the personal consumption expenditures (PCE) price index rose 4.1% YoY, a new high since 2023; core inflation excluding food and energy increased 3.4%. Service inflation excluding housing has almost not declined.

A detail in the minutes worth noting: a minority of participants believed that the June meeting “had sufficient reasons to hike,” yet they ultimately supported holding rates steady. This indicates that the divergence reflected more about differing outlooks for the future rather than disagreement over current policy actions. But “not raising rates for now” and “not needing to hike” are two different things—markets are learning to distinguish between them.

Another highlight of the minutes is the communication shift led by Warsh. Most officials supported shortening the post-meeting statement and agreed to remove language hinting at the next policy move. The final statement eliminated “forward guidance,” emphasizing instead that policy will depend on future data. This change suggests the Fed is intentionally reducing the informational content of the minutes, and future minutes may no longer clearly indicate the level of support for different policy views.

Key signals from the Fed’s June meeting minutes

AI Inflation: The Birth of a New Macro Variable

This is the most groundbreaking aspect of the minutes.

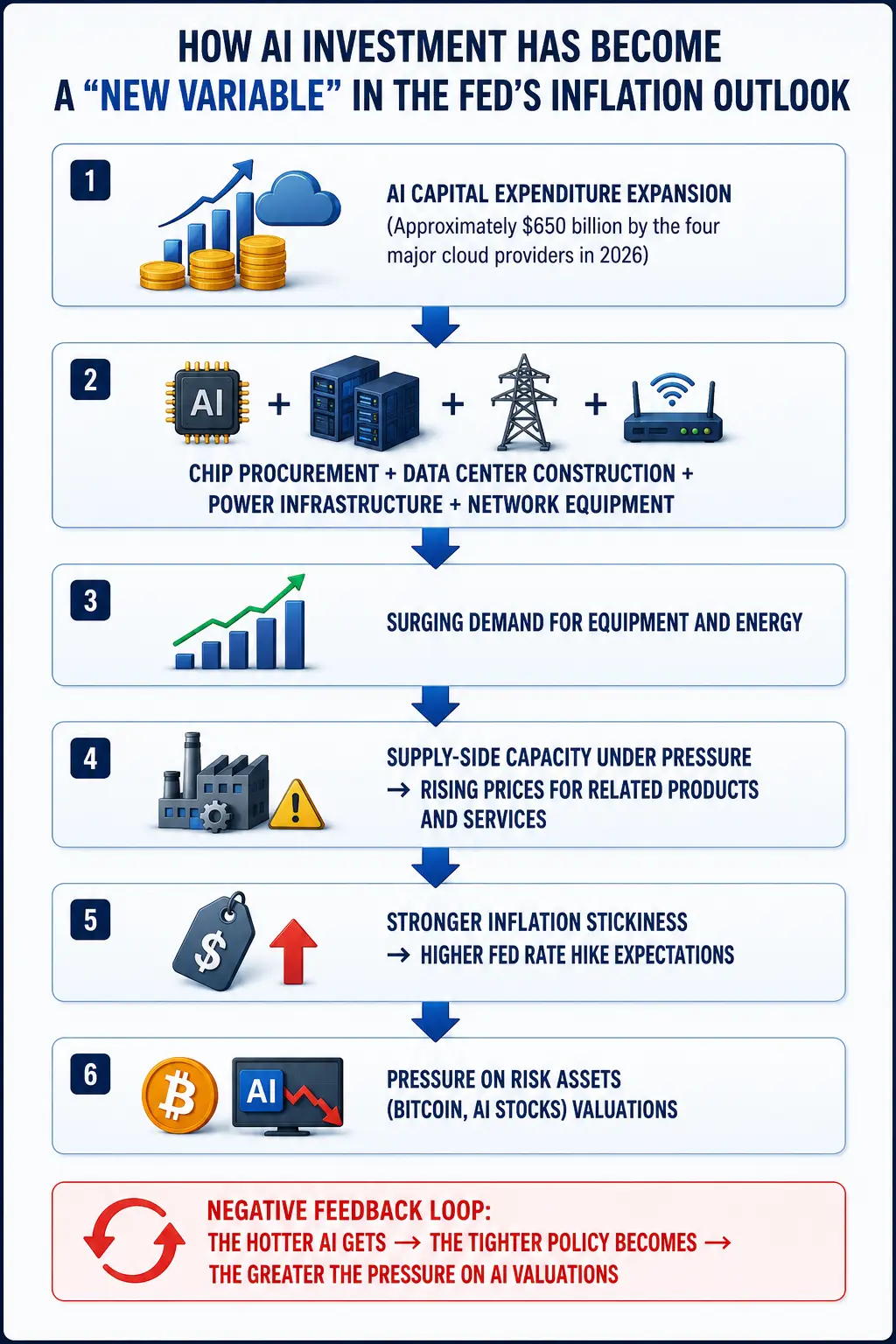

For the first time, the minutes formally included artificial intelligence (AI) investment in the discussion of inflation. Just a few months ago, AI infrastructure investment was hardly a focus of Fed discussions on inflation. Now, it ranks alongside Middle East conflicts and tariffs as one of the three major forces driving inflation higher.

Several officials explicitly pointed out that strong demand for AI infrastructure could push up prices for high-tech products and electricity, thereby intensifying short-term inflation pressures. The minutes state: “Multiple participants commented that price pressures have become more widespread, with most goods and services experiencing significant increases.” More officials believe that robust business investment driven by AI infrastructure could become a new force maintaining price pressures.

This judgment is not baseless. TD Cowen projects that major hyperscale cloud service providers will spend about $745 billion on capital expenditures in 2026, continuing to invest over $1 trillion in 2027 and 2028. According to their estimates, these giants’ spending will reach about 3% of GDP next year, significantly higher than the less than 0.5% level in 2020. The four major U.S. tech giants (Google, Amazon, Meta, Microsoft) forecast their combined capital expenditure will reach approximately $650 billion by 2026.

These funds are highly targeted and physical—chip procurement, data center construction, power infrastructure, network equipment, and building investments. 81% of respondents believe that AI infrastructure development will push up inflation within the next year.

The logical chain from Fed officials is clear and direct: AI capital expenditure expansion → increased demand for equipment and energy → supply capacity pressure → rising prices → sticky inflation. This logic differs fundamentally from energy- or wage-driven inflation—it stems from structural expansion on the corporate investment side, rather than purely consumer demand or supply shocks.

Notably, Warsh has previously stated that AI will, in the long term, help suppress inflation by boosting productivity. But the minutes show that short-term risks are clearly the main concern for officials. As a result, Fed staff have raised their inflation forecasts for 2026 and 2027.

The Fed faces a delicate dilemma: a year ago, officials could have viewed tariff-driven price increases as a “one-off shock” and waited, as the labor market was still sufficiently slack. Now, with stable hiring and new cost pressures from energy and AI, continuing to wait risks entrenching above-target inflation.

How AI investment has become a “new inflation variable” in the Fed’s eyes

Rate Hike Expectations Rise, Short-term Pressure on Bitcoin and Long-term Logic

For crypto markets, the shift in Fed policy expectations is the most direct pricing factor.

According to Gate data, as of July 9, Bitcoin was at $62,045.5, down 1.24% in 24 hours, with a market cap of about $1.24 trillion. Over the past 7 days, it declined 7.63%; over 30 days, down 10.73%; and over the past year, down 33.74%. The 24-hour trading volume was approximately $8,932.97 (note: this is platform display data; actual 24-hour trading volume should be in the tens of billions). Market sentiment remains neutral. The fear and greed index fell to 20–23, indicating “extreme fear.”

Bitcoin briefly dropped below $61,500 after the minutes were released, then rebounded above $62,000. Gate data shows the 24-hour trading range was roughly $61,473 to $63,706, with volume below the recent 20-day average. The 1-hour price was close to the MA20 at about $62,175 but still below the MA50 at approximately $62,932.

In the short term, the rising rate hike expectations suppress crypto assets through three channels:

-

US dollar strength. Expectations of rate hikes generally support the dollar index. Data shows that in the first half of 2026, Bitcoin’s negative correlation with the dollar index is very high, around -0.85. A stronger dollar directly pressures Bitcoin.

-

Rising US Treasury yields. After the minutes, the two-year US Treasury yield increased. The rise in risk-free rates reduces the relative attractiveness of risk assets, putting valuation pressure on BTC and ETH.

-

Shrinking risk appetite. Bitcoin has fallen from about $126,000 at the end of 2025 to around $62,000 in July 2026, a decline of approximately 50.8%. Higher interest rates—even just the credible threat of hikes—tighten liquidity across financial markets.

CME FedWatch shows that the market assigns a 74.3% probability to holding rates steady in July, and a 25.7% chance of a 25 basis point hike. By September, the probability of no change drops to 42.9%, with a 46.2% chance of a 25 basis point hike and 10.8% for a 50 basis point hike. The market is pricing in one or more rate increases. Former St. Louis Fed President Jim Bullard openly stated that a single adjustment is meaningless, and a full tightening cycle is highly likely. Bank of America also raised its forecast, expecting the Fed to hike three times this year, each by 25 basis points.

However, short-term pressure does not necessarily mean long-term bearishness. The minutes also contain a potentially overlooked detail: Fed staff’s GDP growth outlook is only slightly below April’s forecast—indicating no substantial deterioration in economic fundamentals. If AI-driven capital expenditure expansion indeed improves corporate profits and economic growth, institutional funds could flow back into crypto via ETFs. In fact, on July 7, Bitcoin spot ETF saw net inflows of $21.43 million for three consecutive days, ending a streak of 10 days of net outflows totaling $2.7 billion. ETH spot ETFs also experienced four days of net inflows.

From a broader macro perspective, the long-term valuation of crypto assets depends not only on policy directions but also on the total and structure of global liquidity. If AI-driven growth ultimately raises the global real interest rate, all risk asset valuations will undergo a restructuring—Bitcoin cannot be immune, but it also doesn’t necessarily collapse.

Rebuilding AI Stock Valuations: From Frenzy to Rationality

Alongside crypto, AI concept stocks are also under pressure. After the minutes, semiconductor and AI-related stocks were sold off.

Nvidia has fallen about 14% from its May high. Since 2026, Nvidia’s stock has only increased 5.6%, lagging behind the 9.6% gain of the S&P 500 and the 16% rise of the Nasdaq 100. Its market cap has evaporated about $1 trillion since the peak on May 14. Its P/E ratio has returned to 18, pre-AI boom levels, below the S&P 500’s 21. AMD has fallen about 11.5% from its June 30 high, with an 11% decline since July. Applied Materials dropped about 22% from its June 30 high; Micron retreated 24% since June 25.

On July 9, Nvidia rebounded 3.65%, Broadcom rose 4.83%, and the Philadelphia Semiconductor Index gained 0.8%—but these rebounds are modest compared to previous declines.

Multiple institutions are aligned: Goldman Sachs believes the market has entered a “selective stock picking phase”; JPMorgan emphasizes that demand for AI chips remains long-term unchanged; Bank of America sees several more years of growth in the AI cycle. But the market logic is shifting from “valuation-driven” to “profit-driven”—further gains in AI stocks will require actual performance, not just narratives.

The minutes also reveal a deeper contradiction: if AI investment indeed pushes up inflation and forces the Fed to hike, then the valuations of AI stocks will be negatively impacted by liquidity tightening. This is a self-limiting effect of AI as an “inflation driver”—the hotter AI gets, the tighter policy becomes, and the greater the valuation pressure on AI stocks. Whether this negative feedback loop will interrupt the expansion of AI capital expenditure is one of the most important macro issues to watch over the next 12 to 18 months.

A New Investment Framework: How AI-driven Inflation Reshapes Asset Allocation Logic

The June meeting minutes go beyond a single policy event; they mark a structural expansion in the Fed’s discussion framework—AI is no longer just a tech sector topic but a core variable in macro policy formulation.

In the coming years, a new transmission chain may form: AI investment expansion → increased capital expenditure → rising demand for equipment and energy → inflation structure change → Fed policy path adjustment → impacts on US stocks, gold, Bitcoin, and global liquidity.

For investors, this means the traditional “rate hikes = risk asset declines” formula may no longer hold. The AI-driven capital expenditure cycle has a dual nature: it can “push up inflation (bearish for liquidity)” and “improve growth (bullish for profits).” The ultimate outcome depends on which force dominates.

The next Fed meeting is scheduled for July 28–29. Before that, the July 14 CPI data will be a key reference. Warsh will testify before the Senate Banking Committee on July 15. These events will provide more clues about the policy path.

Until the data is clearer, the market is likely to continue oscillating between $61,500 and $63,000. But one thing is already clear: AI has officially become part of the macro narrative, and the crypto market needs to reprice under this new policy framework.

Conclusion

The June Fed meeting minutes marked the first time AI investment was included in the inflation risk list, signaling a structural expansion of macro policy discussion. Nine officials expect rate hikes within the year, and the median dot plot forecast was raised to 3.8%, with the rate cut narrative being replaced by hike expectations. In the short term, Bitcoin faces pressure from a stronger dollar, rising US Treasury yields, and shrinking risk appetite—Bitcoin has fallen about 50% from its high and is currently oscillating near $62,000. However, ETF net inflows and improved growth expectations driven by AI still leave room for long-term resilience. The July CPI data and the upcoming FOMC meeting at month’s end will be key nodes. Until then, markets will seek a new equilibrium within this framework.

FAQ

Q: What is the core signal of the Fed’s June meeting minutes?

The minutes show significant internal disagreement within the FOMC about the future rate path. Although June’s decision was to keep rates at 3.50%-3.75% unanimously, 9 of 18 officials expect at least one hike before the end of 2026. Market focus has shifted from “when to cut” to “whether to hike again.” The minutes also for the first time list AI investment as one of the three major risks pushing inflation higher.

Q: Why does the Fed see AI investment as an inflation risk?

AI infrastructure investment is massive—major cloud providers are expected to spend about $745 billion in 2026. The surge in demand for chips, data centers, electricity, and related products is driving up prices, creating demand-pull inflation. Fed officials believe this structural investment boom could make inflation more sticky, influencing the monetary policy path.

Q: How did Bitcoin perform after the minutes were released?

Bitcoin briefly dropped below $61,500, then rebounded above $62,000. As of July 9, it was at $62,045.5, down 1.24% in 24 hours, with a market cap of about $1.24 trillion. Over the past 7 days, it declined 7.63%; over 30 days, down 10.73%; and over the past year, down 33.74%. The market sentiment remains neutral to weak.

Q: Does Fed rate hikes necessarily mean Bitcoin will keep falling?

Not necessarily. In the short term, rate hike expectations do suppress risk assets. But in the long term, if AI investment boosts economic growth and corporate profits, institutional funds could flow back into crypto via ETFs. On July 7, Bitcoin spot ETF saw three consecutive days of net inflows, ending a 10-day outflow totaling $2.7 billion. Crypto asset prices depend on overall global liquidity and structure, not just policy moves.

Q: Is there still room for AI stocks to rise?

Many institutions believe the long-term trend remains intact, but the market is shifting from “valuation-driven” to “profit-driven.” Leading stocks like Nvidia have pulled back significantly from their highs, with valuations returning to pre-AI boom levels. Future gains will require actual performance, not just narratives. The negative feedback loop between AI investment and liquidity tightening will be a key macro factor to watch.