MicroStrategy (Strategy) announced year-to-date performance data on the X platform on April 7, revealing that its Bitcoin accumulation speed has significantly surpassed the amount of new Bitcoin issued by the network. Year to date, MicroStrategy has bought 94,470 BTC, equivalent to 2.2x the network’s year-over-year new issuance during the same period after the 2024 halving. Chief executive officer Michael Saylor warned that 2026 may be the “last window” when Bitcoin is below $100,000.

The Significance of the Supply Absorption Multiple: The Calculation Behind 2.2x

After the 2024 Bitcoin halving, each mined block produces 3.125 BTC. With the network averaging about 144 blocks per day, that’s about 450 BTC entering circulation daily. Based on an accumulation period of roughly 90 to 100 days, the total new issuance amounts to approximately 40,000 to 45,000 BTC.

MicroStrategy’s year-to-date purchase of 94,470 BTC far exceeds the new issuance in the same period, bringing its supply absorption multiple to 2.2x. This means MicroStrategy not only absorbs all newly mined Bitcoin in the market, but also continues to consume exchange-held stock liquidity. Saylor summarizes this dynamic using a “supply absorption” framework, stating: “We can buy more Bitcoin than they can sell.”

Year-to-Date Financial Performance: BTC Yield and Valuation Data Summary

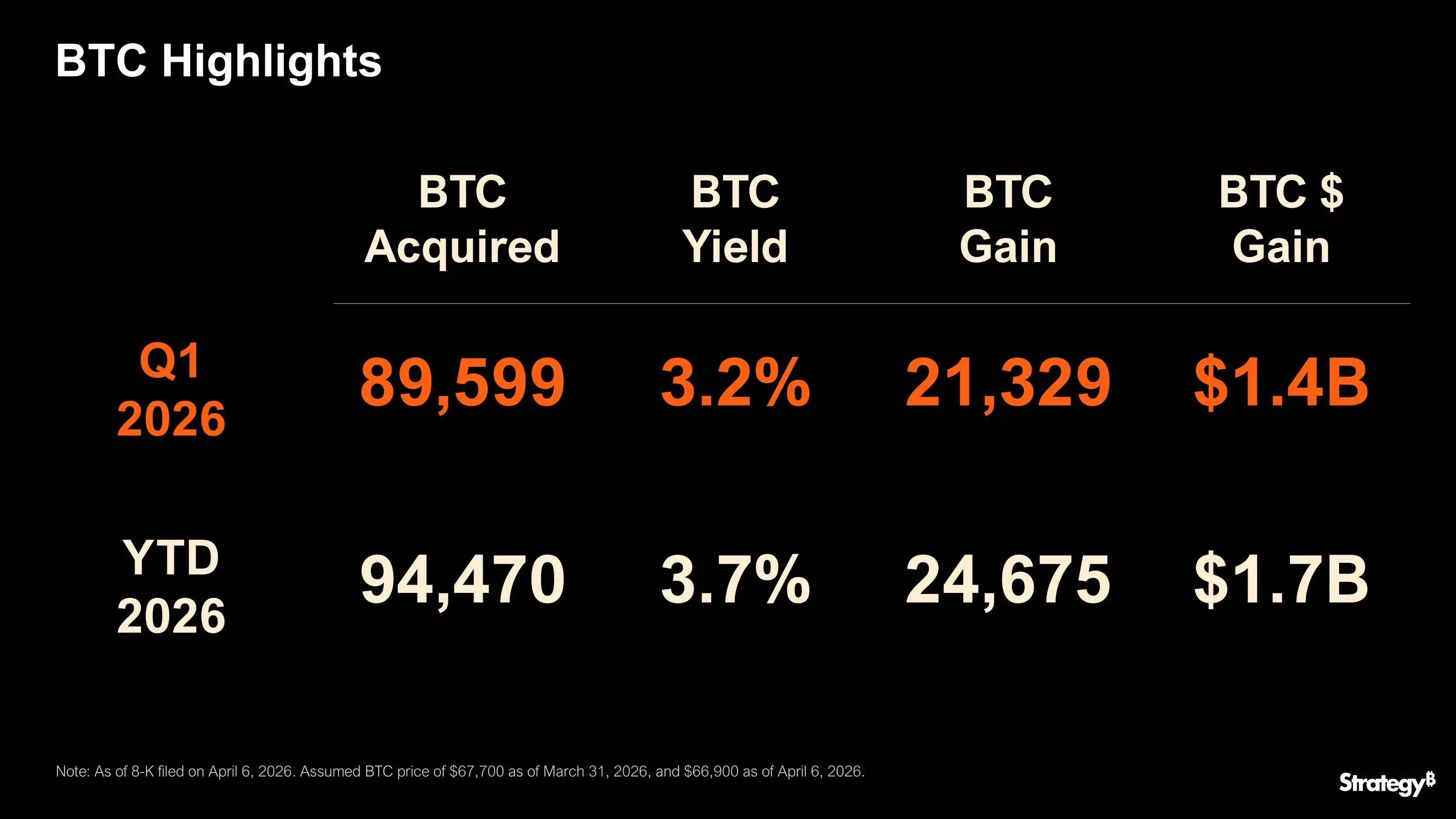

In this update, MicroStrategy provided detailed performance comparison data for year to date and Q1 2026.

MicroStrategy Bitcoin Performance Highlights (2026)

Q1 2026 Purchase Volume: 89,599 BTC, BTC yield of 3.2%, generating 21,329 BTC in appreciation, corresponding to approximately $1.4 billion in appreciation

Year-to-Date Purchase Volume: 94,470 BTC, BTC yield of 3.7%, generating 24,675 BTC in appreciation, corresponding to approximately $1.7 billion in appreciation

Supply Absorption Multiple: Year-to-date purchase volume equals 2.2x the network’s new issuance during the same period

MicroStrategy’s market positioning data is also worth noting: share price $123.63 (down 3.18% daily), market cap $42.88 billion, enterprise value $59.17 billion, and the mNAV ratio of 1.13 indicate that its stock valuation is modestly higher than the net asset value of its Bitcoin holdings; the 36% amplification factor reflects a high correlation between stock performance and the underlying Bitcoin position.

Saylor’s “reflexive flywheel” effect and 2026 market outlook

Saylor describes MicroStrategy’s Bitcoin accumulation mechanism as a “reflexive flywheel”: continuous capital inflows allow it to purchase Bitcoin at a pace that exceeds new issuance, continuously compressing available market supply and forming ongoing absorption of exchange liquidity, which in turn affects the Bitcoin supply-and-demand structure. He further characterizes Bitcoin as a digitized scarce asset with “limited land area,” emphasizing that a fixed supply cap creates competitive scarcity among different market participants.

Saylor’s view of 2026 is especially noteworthy: “2026 will be the year of the last time people can buy Bitcoin at a price below $100,000.” This statement is based on structural logic—demand continuing to grow, supply fixed, and becoming increasingly scarce.

It is also worth noting that before this update, Saylor had reactivated the industry-well-known “Orange Dot” release pattern. The crypto community generally views this as a precursor signal that MicroStrategy is about to make another round of large-scale Bitcoin purchases.

Frequently Asked Questions

What is MicroStrategy’s BTC yield (BTC Yield)?

BTC yield is MicroStrategy’s custom metric for tracking the efficiency of growth in its Bitcoin holdings. It reflects the percentage of BTC appreciation achieved through market financing and operating activities, assuming that existing shareholders are not diluted in terms of BTC holdings per share. The 3.7% BTC yield since the beginning of 2026 indicates that the number of BTC corresponding to each share has grown by 3.7% versus the start of the year.

What structural impact does MicroStrategy’s supply absorption speed have on the Bitcoin market?

MicroStrategy’s year-to-date purchase of 94,470 BTC equals 2.2x the network’s new issuance during the same period, meaning its buying activity not only absorbs all newly mined Bitcoin, but also continues to consume exchange-held stock liquidity. According to Saylor’s analytical framework, if this trend continues, it could further compress Bitcoin’s market-available supply and strengthen the logic of scarcity-based pricing.

What logic underpins Saylor’s claim that 2026 is the “last window” for Bitcoin below $100,000?

Saylor’s judgment is based on three core logics: Bitcoin’s fixed supply cap (21 million), the continuously declining daily new issuance rate (about 450) following the 2024 halving, and the fact that institutions such as MicroStrategy keep accumulating Bitcoin at a speed far exceeding new issuance—accelerating the compression of market-available supply. This is a long-term assessment of the dual trends of demand growth and fixed supply, not a short-term price forecast.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.