Why Most Asset Tokenization Is Actually a Mapping of Prices and Rights

Many people intuitively believe that asset tokenization means the blockchain truly holds the asset. Yet, at the legal, custody, regulatory, and practical levels, this almost never happens directly.

Stocks, gold, bonds, and foreign exchange in the real world all depend on centralized custody systems and legal ownership registration frameworks. Blockchain cannot replace these systems; it can only map certain rights structures related to these assets onto the chain.

Most On-chain TradFi products essentially involve the following types of mappings:

- Price Mapping: For example, on-chain price contracts for gold, crude oil, and stock indices

- Yield Mapping: For example, yield distribution rights for government bonds and deposit rates

- Settlement Mapping: For example, cash settlement logic when contracts expire

- Credit Mapping: Asset anchoring provided by centralized institutions or custodians

What is held on-chain is not the asset itself, but a contractual claim to an asset’s price or yield. This logic is highly similar to futures and CFDs, except that settlement and execution have moved from traditional clearinghouses to smart contracts.

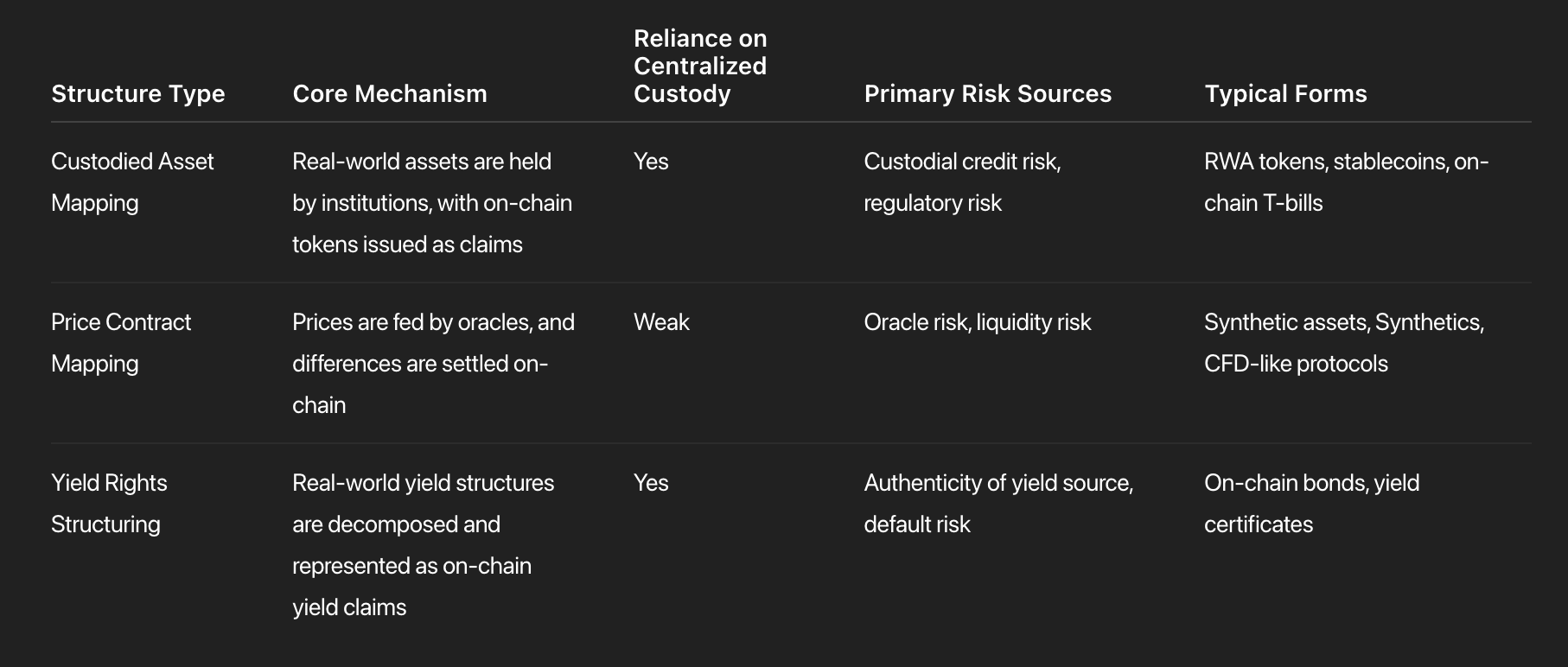

Three Main Structures and Risk Differences of On-chain TradFi

In actual product design, On-chain TradFi has developed three main structures. They may appear similar, but their sources of risk are entirely different.

We can see:

- The first type is closest to asset tokenization but still fundamentally relies on centralized credit.

- The second type is most decentralized but only maps prices without involving assets.

- The third type falls in between, emphasizing cash flows and yield distribution.

These three models are not a matter of superiority or inferiority but are choices of different risk transfer paths.

Why Crypto Markets Are More Suitable for TradFi Derivatives

A highly counterintuitive conclusion is: blockchain is not well-suited to carrying TradFi spot assets but is extremely well-suited for TradFi derivative structures.

The reason is that crypto markets inherently possess several conditions that traditional markets lack:

- 24/7 continuous trading

- Fully on-chain margin and automatic settlement

- Permissionless global liquidity access

- Smart contracts that automatically execute mark-to-market and risk controls

- Highly standardized asset representation (Token)

These features align closely with the operational logic of derivatives such as futures, options, CFDs, and swaps.

In traditional markets, derivatives rely on complex clearing institutions, margin systems, and manual risk control; on-chain, these can be automated through code.

Therefore, we see a trend:

- Tokenizing stocks faces numerous challenges

- US Treasury tokenization depends heavily on strong custody

- Yet on-chain synthetic stock index, FX, and gold price protocols are growing rapidly

Because what blockchains excel at is not holding assets themselves, but efficiently handling price volatility, margin logic, and settlement mechanisms.