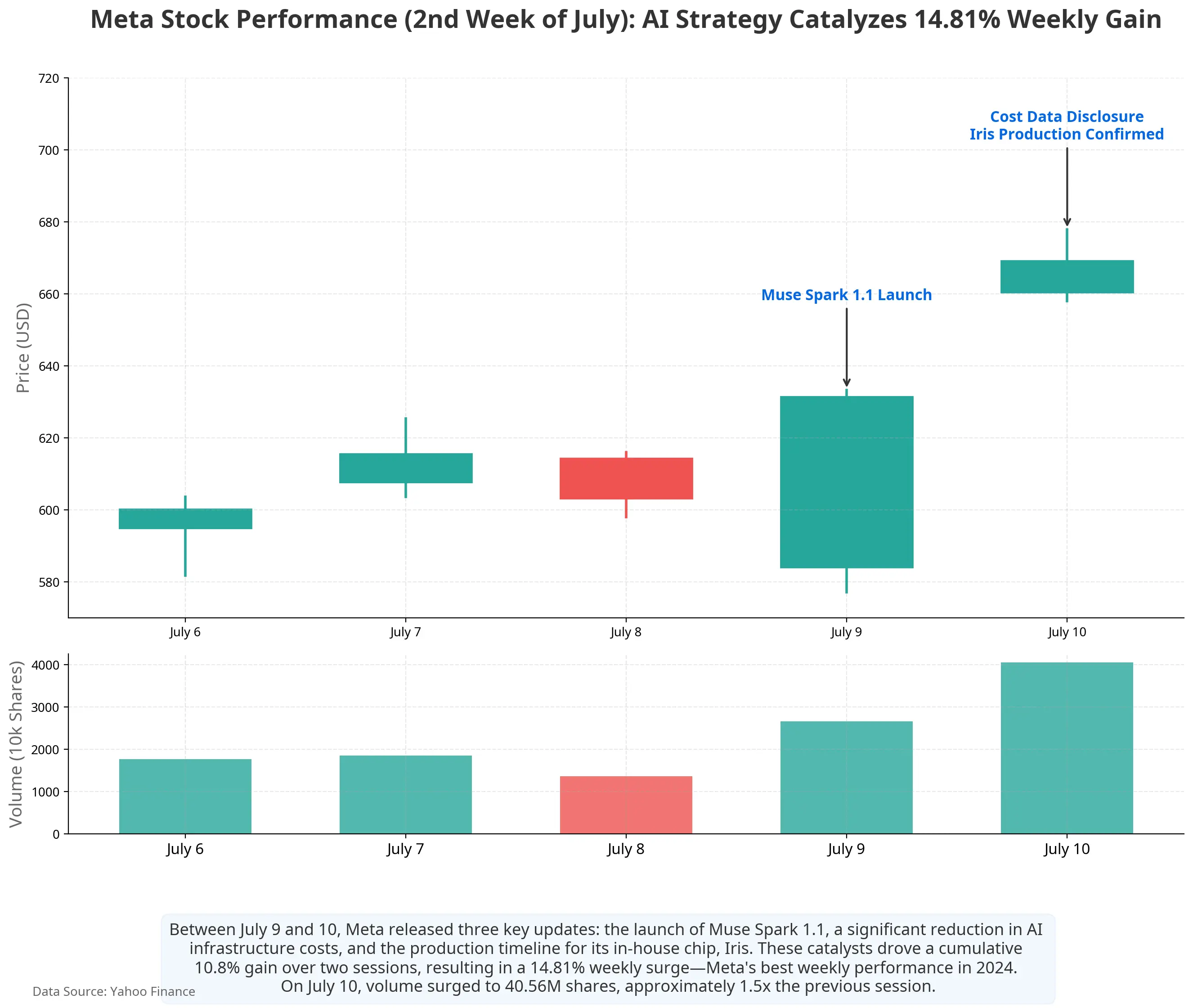

The backdrop for this rally is quite unusual. Just a week earlier—on July 1—news that “Meta plans to sell off excess AI computing capacity” sparked widespread market concerns about “AI compute oversupply,” putting pressure on some AI infrastructure-related stocks. However, within just a few days, the narrative quickly reversed. From July 9 to July 10, Meta released three major AI strategic updates in quick succession: unveiling its next-generation multimodal reasoning model Muse Spark 1.1 and first opening a paid API to developers; disclosing that construction costs for its AI infrastructure unit have dropped significantly; and confirming that its in-house AI chip Iris will move into mass production in September.

Taken together, this series of updates points to a core question: Meta is gradually transforming AI infrastructure that was previously viewed as a “cost center” into business units that can generate revenue. From three dimensions—stock-price drivers, the AI commercialization path, and capital expenditure efficiency—this piece analyzes the market’s logic for re-pricing Meta’s AI strategy.

Meta stock price recent chart

Muse Spark 1.1 launch: from internal tool to sellable asset

On July 9, Meta’s Superintelligent Laboratory officially launched Muse Spark 1.1. This is a multimodal reasoning model designed specifically for agent tasks, with notable improvements over its predecessor in tool calling, computer use, code development, and multimodal understanding. The model supports a 1 million token context length and can retain key information throughout long-running workflows. For agent collaboration, Muse Spark 1.1 uses an architecture in which a main agent collects information, formulates plans, then splits tasks to multiple sub-agents that execute in parallel.

Equally important as the model itself is the change in how it is released. This is the first time Meta has opened model access to developers via the Meta Model API, which is currently in public preview. More importantly, Muse Spark 1.1 introduces paid tiers for developers—Meta’s first paid business model for an AI model. Meta CEO Mark Zuckerberg said the API pricing for the model will be among the lowest in the market, at about 25% of the pricing of OpenAI and Anthropic’s top-tier models.

The significance of this change is that Meta’s AI models finally have a direct external revenue path. Previously, Meta’s AI capabilities mainly served ad recommendations and content distribution within its internal ecosystems such as Facebook, Instagram, and WhatsApp. The market had long been unable to answer how “tens of billions of dollars” in AI spending produce returns. The paid API for Muse Spark 1.1 and the opening of the Meta Model API provide the first piece of the puzzle—model call fees and enterprise AI service revenue.

Compute: from cost to asset—rebuilding the logic of infrastructure commercialization

The launch of Muse Spark 1.1 is only part of Meta’s AI commercialization narrative. The larger logic shift is happening at the infrastructure layer.

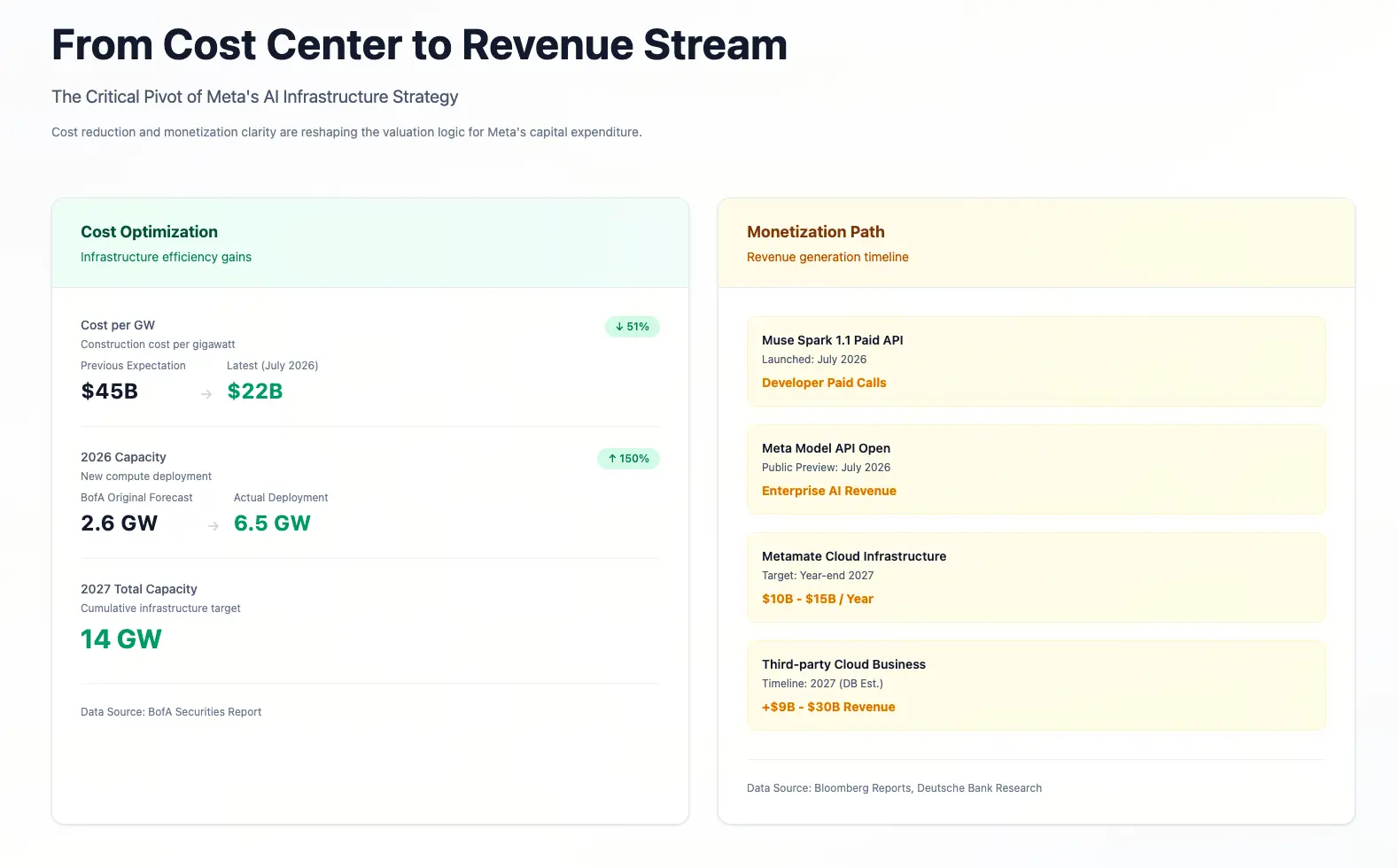

For the past two years, the market’s main concern about Meta’s AI strategy has centered on a single number: capital expenditure. In 2025, Meta’s full-year capital expenditures were about $72.2 billion. In January 2026, the company set its full-year capital expenditure guidance at $115 billion to $135 billion. After its first-quarter earnings report in April, that range was raised again to $125 billion to $145 billion. Based on the midpoint, Meta’s year-over-year increase in 2026 capital expenditures is about 88%. Investors have repeatedly asked the same question: when will the money spent start paying back?

In July 2026, the market’s framework for answering this question is changing.

First, there is a major optimization in unit costs. In a July 10 report, Bank of America analyst Justin Post said that, based on Meta’s disclosed 2026 deployment plan and a $145 billion capital expenditure budget, the unit construction cost of Meta AI’s compute capacity has fallen from the previously estimated $45 billion per GW to about $22 billion per GW. Meta plans to add 6.5GW of compute capacity in 2026. A 50% cost reduction means the same amount of capital can support twice the scale of compute previously expected.

Second, revenue visibility is improving. According to Bloomberg, Meta is putting together a cloud infrastructure business unit, tentatively named Metamate, aiming to generate at least $10 billion to $15 billion in annual revenue by the end of 2027. In a July 10 research note, Deutsche Bank further estimated that if annual revenue per GW is $10 billion to $15 billion, Meta’s third-party cloud business in 2027 could contribute about $14.6 billion to $36 billion in incremental revenue.

This logic is structurally similar to the growth path of Amazon AWS—turning redundant infrastructure built internally to support the core business into an external service that generates revenue. But there is an important difference at the starting point: AWS emerged from compute surplus tied to Amazon’s e-commerce business, while Meta’s compute pool was built to support its ad business and AI model training. The scale of this pool far exceeds internal needs—Meta’s pledged future AI infrastructure investment already reached $182.9 billion as of the end of Q1—so selling idle compute externally becomes a feasible path to absorb fixed costs.

In-house chip Iris: a hardware plan to reduce long-term costs

In the logic chain for lowering long-term AI infrastructure costs, in-house chips are another key piece of the puzzle.

According to an internal Meta memo reviewed by Reuters, the company plans to begin mass production of its in-house AI chip, code-named Iris, in September 2026. The chip is part of Meta’s fourth-generation training and inference accelerator program. Meta designs it in-house, Broadcom assists with the design, and TSMC handles manufacturing. Testing took only 6 weeks and found no major issues—an important milestone for an in-house chip initiative that has been underway for more than 5 years and progressed slowly at one point.

Iris is not positioned to fully replace Nvidia GPUs, but to complement them. The memo states that for a company the size of Meta, adopting the latest GPUs “has always been a difficult task and takes a lot of time.” The core value of an in-house chip is: reducing dependence on a single supplier, optimizing the cost structure of inference, and improving the overall efficiency of the infrastructure.

From the perspective of capital expenditure efficiency, Iris’s mass production helps improve the key metric of “how much compute can be generated per $1 invested.” If the unit cost of in-house chips is better than that of purchased GPUs for inference tasks, then the same scale of capital expenditures can support more effective compute output, thereby expanding the infrastructure commercialization profit margin.

Market reaction and analyst re-pricing

After this set of information was released, Wall Street analysts quickly adjusted their valuations.

As of July 13, data compiled by MarketBeat showed Meta’s average 12-month target share price is about $840.64, with the highest target at $1,015. Bank of America maintained a Buy rating with a target price of $835; Deutsche Bank maintained a Buy rating with a target price of $810; Piper Sandler maintained a Buy rating (upgrading to Overweight) with a target price of $800; and Jefferies maintained a Buy rating with a target price of $825. At the current share price of $669.21, there is still about 25.6% upside versus the average target price.

But the disagreement is also clear. Some institutions are concerned about continued expansion in capital expenditures. Citizens Bank cut its Meta target price to $800, citing pressure brought by increased capex. While Wolfe Research kept a “outperform” rating, it raised its forecast for capital expenditures for fiscal 2027 to $220 billion. FactSet estimates that Meta may record negative free cash flow of more than $1 billion in the second quarter of 2026.

Meta AI infrastructure costs and commercialization path comparison

Conclusion

Meta’s stock rise in the second week of July 2026 reflects the market’s re-pricing of its AI strategy narrative. The paid API for Muse Spark 1.1, the opening of the Meta Model API, Iris’s mass production timeline, and the sharp drop in unit costs for AI infrastructure—all point to a single direction: Meta is shifting from being an “AI investor” to an “AI service provider.”

Whether this shift can continue to support the valuation depends on three verifiable metrics: Metamate’s customer acquisition progress and revenue growth rate, the actual improvement in inference costs from the in-house chip, and changes in advertising profit margins with AI enhancements. Over the coming quarters, the market will no longer be satisfied with the narrative of “Meta building AI”—it will demand evidence that “AI is generating revenue.”

For investors, the core question is not whether Meta should invest in AI, but whether Meta’s AI investment efficiency is better than that of competitors. On this point, cost data ($22 billion per GW versus the previously estimated $45 billion) and the commercialization timeline (a $10 billion to $15 billion revenue target in 2027) provide a preliminary reference framework. But the real answer will only unfold gradually through future quarterly earnings reports.

FAQ

Q: What are the main reasons for Meta’s recent stock increase?

Meta shares closed at $669.21 on July 10, up 5.97% on the day, with a total weekly gain of about 14.8%. Key drivers include: the release of the Muse Spark 1.1 model and the first opening of a paid API; AI infrastructure unit construction costs falling from $45 billion per GW to $22 billion; and the in-house AI chip Iris confirming September mass production. Together, these three changes altered market expectations for Meta’s AI investment payback cycle.

Q: How large is Meta’s AI capital expenditure?

Meta’s full-year capital expenditures in 2025 were about $72.2 billion. Meta’s 2026 capital expenditure guidance is $125 billion to $145 billion, raised versus the guidance at the start of the year. As of the end of Q1, Meta has already committed to $182.9 billion in future AI infrastructure investment. The company plans to add 6.5GW of compute capacity in 2026, bringing total capacity to 14GW in 2027.

Q: How is Muse Spark 1.1 different from prior models?

Muse Spark 1.1 is Meta’s first paid AI model for developers. It is a multimodal reasoning model supporting a 1 million token context length and featuring multi-agent collaboration capabilities. Developers can call the model via the Meta Model API, with pricing at about 25% of OpenAI and Anthropic’s top-tier models. This is an important milestone in Meta AI’s shift from internal tool to a commercial product.

Q: What is the significance of Meta’s in-house AI chip Iris?

Iris is an AI chip designed by Meta itself, with Broadcom assisting in the design and manufactured by TSMC; it is planned for mass production in September 2026. Its significance lies in reducing dependence on Nvidia GPUs, optimizing the cost structure of inference, and improving the overall efficiency of the infrastructure. The chip passed testing in just 6 weeks, which is a meaningful development for an in-house plan that has been underway for more than 5 years.

Q: What major risks does Meta face in AI commercialization?

Major risks include: AI revenue growth may be lower than capital expenditure growth—annual investment of $125 billion to $145 billion is far higher than current expectations for AI business revenue; competition in AI model services and cloud computing is intense, requiring Meta to compete for customers with established players such as OpenAI, Google, and AWS; and depreciation pressure from large-scale infrastructure investment will continue to weigh on profit margins over the next several years.