Over the past decade, the crypto market has seen the ICO boom, DeFi explosion, NFT rise, and rapid stablecoin expansion. But it has also been plagued by project rug pulls, market manipulation, poor disclosure, and asset security risks. MiCA emerged from this environment, aiming to boost market transparency and investor protection through a unified regulatory framework.

For everyday investors, one key question is which cryptocurrencies MiCA will affect. MiCA does not target any single token. Instead, it builds a rule system covering issuance, trading, custody, and marketing. So whether it's Bitcoin, Ethereum, USDT, USDC, or newly issued project tokens, all may feel MiCA's impact to some degree.

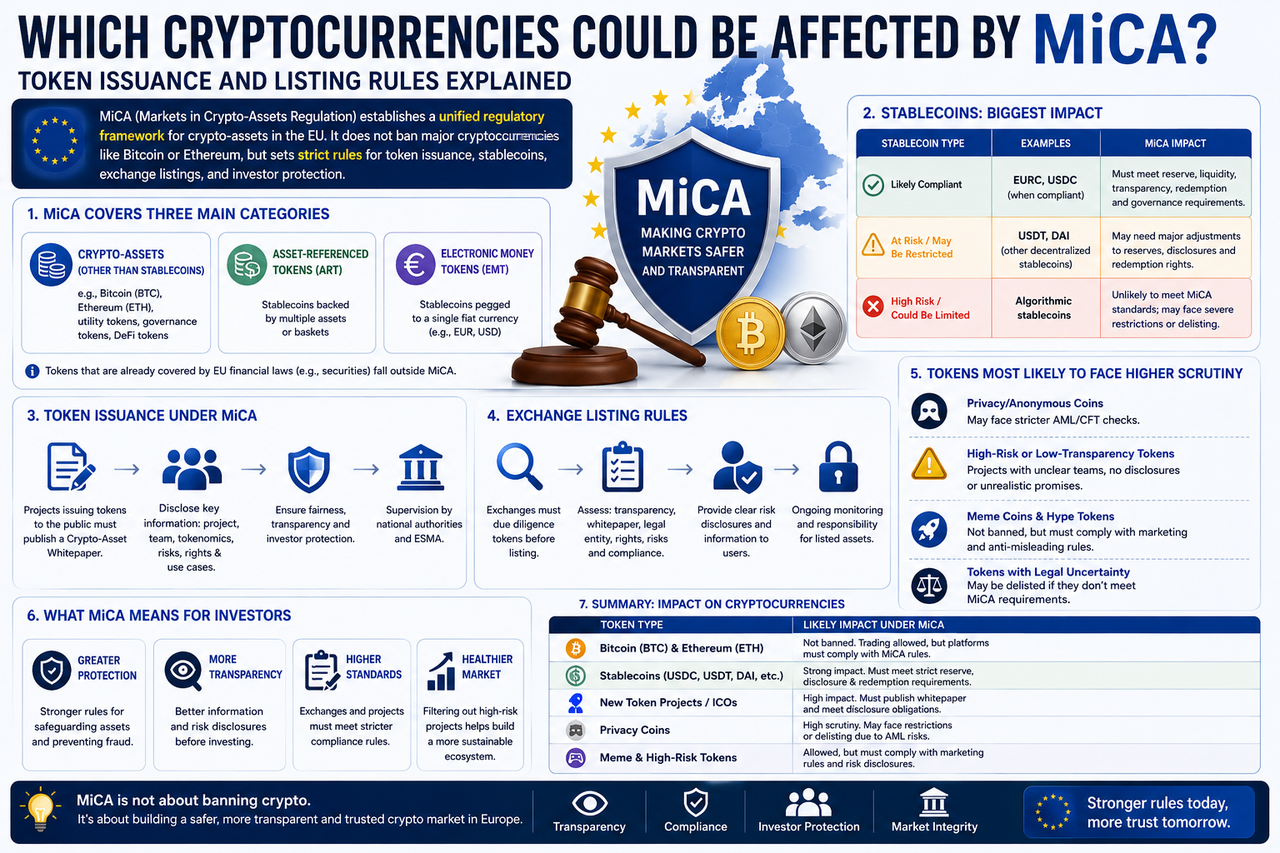

Which Crypto Types Does MiCA Regulate?

MiCA does not treat all digital assets as one product. Instead, it classifies them by attributes for tailored regulation.

Currently, MiCA covers three main categories:

| Asset Class |

Definition |

Representative Projects |

| Crypto Assets |

General digital assets |

BTC, ETH, SOL, AVAX |

| E-Money Tokens (EMT) |

Stablecoins pegged to a single fiat currency |

USDC, EURC |

| Asset-Referenced Tokens (ART) |

Stablecoins pegged to multiple assets |

Some stablecoin projects |

This classification lets regulators set rules based on risk profiles rather than using a one-size-fits-all approach.

Note: MiCA does not apply to security tokens already covered by EU financial laws, so some assets may also fall under other financial regulations.

Will Bitcoin and Ethereum Be Affected by MiCA?

Bitcoin and Ethereum are the two largest crypto assets held by European investors.

Regulation-wise, MiCA will not ban BTC or ETH trading or require users to sell or stop holding them.

However, MiCA will affect their trading environment. For instance, exchanges must disclose asset info, strengthen risk warnings, set up customer asset protection, and meet market transparency rules. When users buy BTC and ETH going forward, most platforms will need CASP authorization.

So MiCA impacts not the assets themselves, but the market participants operating around them.

Which Stablecoins Are Hit Hardest?

Stablecoins are a key MiCA focus.

Because stablecoins serve as the infrastructure for payments, trading, and liquidity in crypto, EU regulators see them as a potential systemic risk source. MiCA requires stablecoin issuers to meet reserve management, audit disclosure, user redemption, and risk control standards.

Stablecoin Regulatory Impact Comparison

| Stablecoin Type |

MiCA Impact Level |

Key Regulatory Requirements |

| USDC |

High |

EMT regulation, reserve disclosure |

| EURC |

High |

EMT regulation, euro reserve management |

| USDT |

High |

Compliance assessment and market restrictions |

| Algorithmic stablecoins |

Very high |

Faces stricter rules |

| Decentralized stablecoins |

Medium to high |

Potential future regulation |

Thus, stablecoins are likely the asset class most visibly affected by MiCA.

Will MiCA Affect New Token Launches?

A host of past ICO projects raised public funds with poor disclosure. MiCA aims to fix that through mandatory disclosure rules.

Under MiCA, project teams publicly offering tokens generally must provide a Crypto Asset Whitepaper detailing goals, tech architecture, risk factors, token use, team background, and investor rights—much like a prospectus in traditional markets. This will make project fundraising more transparent but also raise the bar for token issuance.

How Does MiCA Affect Exchange Listing Rules?

For exchanges, MiCA is reshaping listing logic.

Previously, some platforms prioritized hype and volume. Now regulators emphasize disclosure and investor protection.

When evaluating new assets, exchanges will typically need to confirm basic compliance and supply adequate risk explanations to users.

Key Listing Review Items for Exchanges in the MiCA Era

| Review Item |

Pre-MiCA |

Post-MiCA |

| Project hype |

Core metric |

One metric among many |

| Community size |

Important |

Important |

| Information disclosure |

Inconsistent |

Mandatory |

| Whitepaper quality |

At project's discretion |

Key review focus |

| Risk warnings |

Rare |

Mandatory disclosure |

| Legal liability entity |

Limited requirements |

Clear requirements |

This means the European listing process will increasingly mirror traditional finance standards.

Will Privacy Coins Be Affected by MiCA?

Privacy coins have long been a regulatory focus.

Because some privacy coins offer strong anonymous transfers, they can complicate AML efforts. MiCA does not outright ban privacy coins, but in practice exchanges face stricter compliance. If certain assets make AML reviews difficult, some European platforms may restrict trading or reduce support.

Will Meme Coins and High-Risk Tokens Be Affected?

Meme coins have become market darlings in recent years.

Legally, MiCA does not single out meme coins, but related projects must still follow disclosure and marketing rules. If a project uses misleading ads, promises false returns, or conceals material info, it may face regulatory action.

So MiCA won't ban meme coins, but it may raise the bar for listing on major exchanges.

Are DeFi Tokens Within MiCA's Scope?

This area still has some gray zones.

For tokens issued by fully decentralized protocols, MiCA has no dedicated framework. But if a DeFi project has a clear team, foundation, or business entity, its token issuance and marketing may still face regulatory requirements.

Will MiCA Cause Delistings?

Theoretically, yes.

If an asset fails to meet regulatory standards or its issuer cannot provide necessary disclosure, exchanges may reconsider its listing.

However, most major cryptocurrencies are not expected to be materially affected.

Projects lacking transparency, those without clear responsible entities, high-risk stablecoins, some privacy coins, and legally controversial tokens are more vulnerable. Over time, this screening could improve overall industry quality.

What Does MiCA Mean for Investors?

For ordinary investors, MiCA's biggest impact is greater market transparency.

Going forward, users buying tokens will have easier access to project background, risk info, and issuance details, enabling smarter decisions.

Exchanges will also need to shoulder more user protection and enforce stricter listing reviews.

While some high-risk projects may disappear, overall market safety and standardization should improve.

For long-term investors, this change is generally seen as positive.

Summary

MiCA won't ban Bitcoin, Ethereum, or other major crypto trading, but it will profoundly shape token issuance, stablecoin management, and exchange listing rules. The European market will increasingly prioritize disclosure, investor protection, and transparency. Stablecoins, privacy coins, and some high-risk tokens may face tighter rules.

For projects, MiCA raises the bar for token launches and fundraising. For exchanges, it strengthens listing review duties. For investors, it means a more transparent and orderly market.

FAQs

Will MiCA ban Bitcoin and Ethereum?

No. MiCA will not ban BTC or ETH trading. Its main goal is to regulate market participants and asset issuance.

Which crypto types are most vulnerable to MiCA?

Stablecoins, privacy coins, opaque projects, and some high-risk tokens are most likely to be affected.

Will MiCA affect USDT?

Yes. USDT is a key stablecoin regulatory target and must meet EU reserve management and disclosure requirements.

Will MiCA affect new token launches?

Yes. Token issuers generally need to provide a Crypto Asset Whitepaper and follow disclosure rules.

Will MiCA cause token delistings?

Some non-compliant assets may be re-evaluated or delisted by exchanges, but major crypto is unlikely to be significantly impacted.

Will MiCA affect exchange listing processes?

Yes. Exchanges will focus more on transparency, risk disclosure, legal liability entities, and investor protection. Listing standards may tighten further.