Robinhood’s approach to crypto and on-chain integration addresses how the platform connects to digital assets and executes tokenization, while Robinhood Markets (HOOD) stock concerns how a public company’s equity is priced and disclosed. Though both are part of the same brand narrative, they represent distinct asset classes and risk profiles.

Retail users frequently encounter both stock and crypto options within the same app, often leading to confusion between "company stock HOOD" and "on-chain networks." Clarifying the distinctions among custodial trading, self-custodial wallets, and the Robinhood Chain’s positioning and architecture is essential for understanding this topic.

From the perspective of the crypto industry, brokerages’ crypto operations offer fiat and custodial trading experiences, while Robinhood Chain aims to extend execution and tokenization into composable on-chain environments. For details on revenue impact, see HOOD stock’s business model; for compliance boundaries, refer to HOOD regulation and compliance.

What Crypto Products Does Robinhood Offer?

Robinhood’s public disclosures highlight several crypto features: custodial spot trading and transfers in the US and other markets, localized crypto services in jurisdictions such as Europe, and self-custodial Wallets provided through separate entities. In custodial trading, user assets are held by licensed entities; in Wallet scenarios, users manage their own private keys.

| Form |

Typical Capabilities |

Key Boundaries |

| Custodial Trading |

Spot trading, partial transfers |

Assets held by licensed entity, routed to liquidity providers |

| Self-Custodial Wallet |

Multi-chain access, user controls private keys |

Segregated from brokerage custodial account assets |

| Extended Services |

Staking, perpetuals, etc. (varies by region) |

Availability depends on local regulations |

This table underscores the "different legal and technical containers under a single brand." When reviewing products, users should first confirm account type and jurisdiction, then understand who controls the assets.

How Should You Understand the Wallet vs. Custody Boundary?

Custodial accounts are best for users who want to buy and sell crypto directly using fiat balances. Wallets are intended for those who need on-chain signing and cross-protocol interactions. Robinhood’s disclosures make clear: assets in self-custodial Wallets are not held by the brokerage’s crypto subsidiary, and network gas fees are not collected by the platform (see product documentation for details).

Confusion often occurs when Wallet balances are mistaken for brokerage account holdings, or when HOOD stock positions are confused with on-chain tokens. When trading company equity, verify the NASDAQ ticker HOOD; when managing on-chain assets, check the network, contract, and private key control.

What Is Robinhood Chain? How Is It Positioned?

Robinhood Chain is described in company materials as a permissionless Layer 2 focused on tokenization and on-chain applications. Robinhood Chain’s positioning and architecture explain its role across application scenarios and architecture layers; differences from networks like Base and Arbitrum are covered in Robinhood Chain vs Base vs Arbitrum.

For HOOD stock analysis, Chain is a strategic and ecosystem extension: it may influence Robinhood’s long-term product narrative and crypto-related revenue potential, but cannot replace brokerage revenue, net interest, or subscription analysis in financial statements.

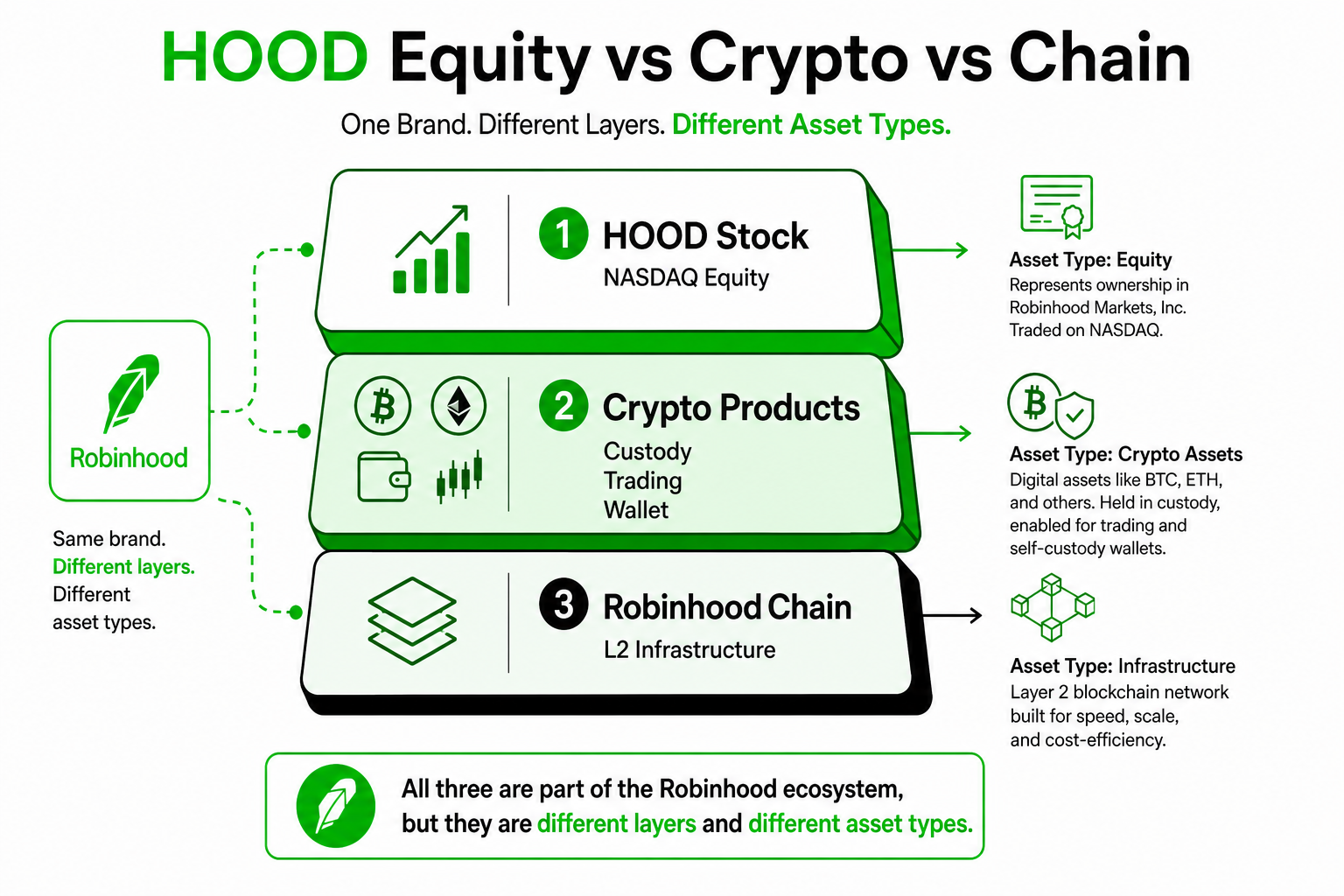

Figure 1. Three-layer distinction: HOOD equity, custodial crypto/Wallet products, and Robinhood Chain infrastructure.

Figure 1. Three-layer distinction: HOOD equity, custodial crypto/Wallet products, and Robinhood Chain infrastructure.

How Are Accounts and On-Chain Execution Connected?

The connection from wallet experience to on-chain execution hinges on account abstraction, signature authorization, and settlement paths. Account and transaction mechanisms detail how users transition from familiar account interactions to on-chain commands. This is a matter of product engineering and chain design, independent of "holding HOOD stock."

Common questions during this process include: who pays for gas and fees, asset bridging risks, and compliance checks when withdrawing from custodial accounts to self-custodial addresses. These factors impact user experience and operational costs, relate indirectly to crypto business competitiveness, but should be discussed separately from equity valuation models.

How Are Security, Compliance, and Transparency Balanced?

Custodial crypto businesses must comply with money transmission, anti-money laundering, and securities regulations; Chain and self-custody scenarios rely more on on-chain verifiability and smart contract security. Security, compliance, and transparency explores how custody, compliance, and on-chain transparency can coexist.

For HOOD shareholders or observers, compliance events, enforcement actions, or major security incidents may affect the company’s reputation and costs, but these are "company-level risks"—not judgments on the validity of specific on-chain transactions. Comparisons with platforms like Coinbase can be found in HOOD vs COIN.

How Should Tokenization Narratives and HOOD Stock Be Understood Together?

Tokenization narratives focus on mapping traditional financial instruments or off-chain rights into forms transferable and settled on-chain. For Robinhood, this is tied to retail access, compliance boundaries, and Layer 2 execution environments, but the mapped assets remain product and infrastructure plans—not HOOD common stock itself.

To understand both in parallel: equity analysis focuses on revenue, user metrics, and regulatory disclosures; tokenization analysis focuses on issuer, underlying assets, redemption/settlement paths, and smart contract risk. Both can be part of a company’s strategy, but represent different rights and default structures.

If tokenization pilots, testnet activities, or partnership announcements are presented as "HOOD fundamentals have changed," it risks skipping over intermediate steps like revenue recognition and licensing. A more prudent approach is to classify such news as product development, then verify in financial statements whether measurable revenue has been generated.

What Are Common Misconceptions?

Misconception 1: HOOD stock is the same as Robinhood Chain tokens or gas tokens—company common stock and on-chain fee tokens are not the same.

Misconception 2: Crypto holdings in the app directly reflect HOOD fundamentals—crypto trading is only one of several revenue drivers.

Misconception 3: Wallet and custodial account risks are the same—self-custody and platform custody have different counterparty structures.

Misconception 4: On-chain browser transaction records can replace brokerage account statements—custodial accounts are still subject to licensing, reporting, and client asset rules.

To clarify misconceptions, focus on four questions: Is the asset equity or on-chain? Is the account custodial or self-custodial? Are we discussing financial results or network parameters? Is the disclosure from investor relations or a block explorer?

Summary

Robinhood’s crypto products offer digital asset trading and transfer, Robinhood Chain extends on-chain and tokenized execution, and HOOD is NASDAQ-listed common stock. These three share a brand but differ in asset types, risk sources, and analytical frameworks. Understanding these distinctions, along with business model and regulatory context, helps avoid conflating on-chain narratives with stock definitions.

FAQ

Does Robinhood Support Crypto Trading?

Yes. Robinhood offers crypto spot and related services through its subsidiaries in applicable jurisdictions. The specific tradable assets and features depend on the local product page and may include transfers, Wallet, or other extended features.

What Is Robinhood Chain? Is It the Same as HOOD Stock?

No. HOOD is the publicly listed stock of Robinhood Markets, Inc.; Robinhood Chain is Layer 2 blockchain infrastructure. Equity and on-chain network analyses should be conducted separately.

How Do Robinhood Wallet and Crypto Trading Accounts Differ?

Crypto trading accounts typically have assets held by licensed entities; Wallet is self-custodial, with users controlling their private keys. This results in different asset control, risk responsibilities, and supported chain networks.

Why Consider Chain When Analyzing HOOD?

Chain is part of Robinhood’s disclosed product and ecosystem expansion and may influence long-term crypto and tokenization narratives, but should not replace analysis of trading revenue, net interest, and subscription items in financial statements.

How Can Custody and On-Chain Transparency Coexist?

Custody businesses rely on licensing, audits, and compliance processes; on-chain activities rely on verifiable transactions and contract logic. Robinhood’s approach emphasizes using the right transparency tools for each product type, rather than applying a single model to all scenarios.