Robinhood Markets (HOOD) stock’s business model explains how the company transforms retail brokerage and related services into reportable revenue, rather than focusing solely on the “zero commission” feature promoted in the App interface. Robinhood Markets (HOOD) is defined by its corporate structure, comprehensive product lineup, and Gate trading path overview. This article highlights how the three revenue pillars and the product matrix reinforce each other.

Retail broker revenue is shaped by trading activity, interest rate environment, and subscription penetration. By examining transaction-based revenue, net interest, and Gold separately, you can better understand HOOD’s flexibility under varying market conditions and compare its framework to pure crypto platforms, as seen in HOOD vs COIN.

When digital assets intersect with public markets, the product matrix determines what users can trade, while revenue categories define what is recognized in shareholder reports. These are related but distinct; order execution should always reference the rules on the Gate Buy HOOD page.

What are HOOD’s three pillars of revenue?

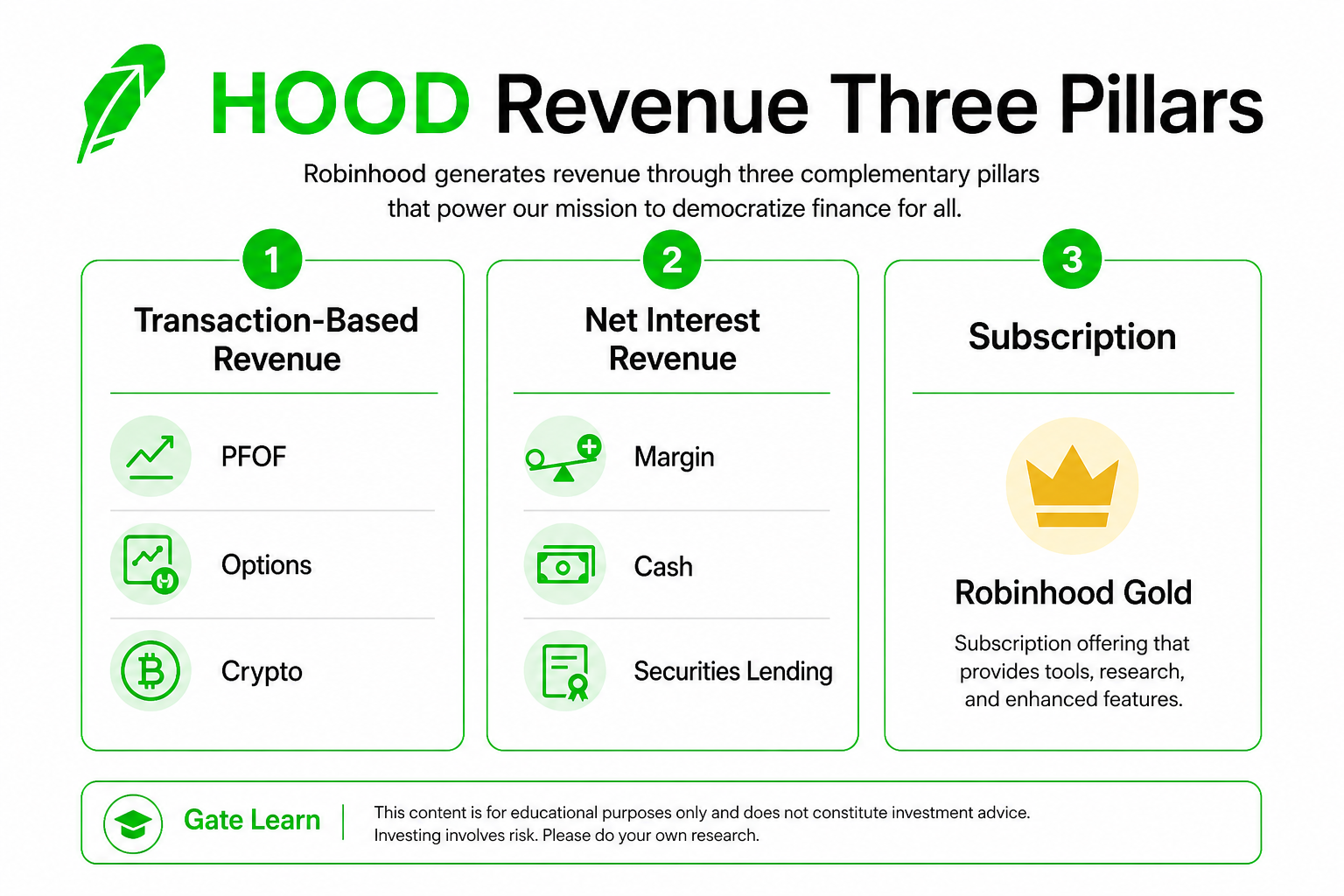

HOOD’s revenue structure consists of three main categories: transaction-based revenue, net interest revenues, and subscription and other revenues. Transaction-based revenue includes income from order execution, routing compensation, and multi-asset trades; net interest covers earnings from customer cash, margin, and securities lending; subscription revenue is primarily generated from membership fees like Robinhood Gold.

| Revenue Type |

Main Source |

Key Drivers |

| Transaction-based |

PFOF, fees for options/crypto |

Trading activity, asset mix |

| Net interest |

Margin, cash balances, securities lending |

Interest rates, cash and lending volume |

| Subscription/Other |

Robinhood Gold, etc. |

Subscriber count, benefit mix |

This table shows each revenue type is influenced by different factors. When reviewing financial reports, first confirm the revenue category, then analyze which type drives quarterly fluctuations.

What is PFOF? How is order routing compensation understood?

Payment for order flow (PFOF) is compensation brokers may receive when routing client orders to market makers or execution venues. Robinhood’s disclosures clarify that transaction-based revenue is tied to order routing and trading activity, with its routing system prioritizing counterparties based on execution quality.

PFOF is not the same as “users paying stock commissions to Robinhood.” Instead, it’s a compensation mechanism within market microstructure for retail orders. Regulatory debates around PFOF impact the institutional environment for transaction-based revenue, with details outlined in HOOD Regulation and Compliance.

To understand PFOF, pay attention to execution quality disclosures, asset class differences (stocks, options, crypto may have distinct routing rules), and the relationship between “zero commission” and “revenue source transfer.”

How does net interest revenue arise?

Net interest revenue represents the interest spread or related earnings from activities like client funds, margin lending, and securities lending. When clients hold idle cash, use margin, or the platform conducts securities lending, both the interest rate environment and balance volume affect this revenue.

Net interest is driven differently than transaction-based revenue: even if trading slows, as long as balances and lending structures persist, net interest can still contribute. Conversely, declining rates may compress this category. Avoid equating net interest with “user interest rewards” or “bank deposit rates.”

What does Robinhood Gold subscription include?

Robinhood Gold is a subscription service for eligible users, offering a suite of value-added benefits for a monthly fee. These typically include higher margin limits, research and data tools, cash interest-related perks, and credit product eligibility within the Gold ecosystem. The exact benefit mix depends on the product page and agreement, and may vary by region and account type.

The value of analyzing subscription revenue lies in its recurring nature: compared to single trades, membership fees better reflect user retention and willingness to pay. When Gold benefits extend to joint accounts or credit card scenarios, subscription fees should be distinguished from bank partnership products’ interest and reward logic.

Figure 1. HOOD’s three revenue pillars: transaction-based revenue, net interest revenue, and Gold subscription.

Figure 1. HOOD’s three revenue pillars: transaction-based revenue, net interest revenue, and Gold subscription.

How does the product matrix support the business model?

The product matrix is the “front end” of the revenue structure: stocks and ETFs provide the basic investment entry; options and futures boost trading density for active users; event contracts expand alternative risk exposure; crypto products introduce digital asset cycles; Gold and Strategies transform one-time trades into ongoing relationships.

| Product Layer |

Key Offerings |

Revenue Relationship |

| Core Brokerage |

Stocks, ETFs |

Order routing, platform asset scale |

| Derivatives |

Options, futures, event contracts |

Increase transaction-based revenue density |

| Crypto |

Spot trading, transfers, Wallet |

Crypto transactions, expanded services |

| Subscription/Advisory |

Gold, Strategies |

Recurring fees, asset allocation |

For details on crypto and on-chain integration, see HOOD Crypto and Robinhood Chain. A broader product offering diversifies revenue drivers but also increases compliance and operational complexity.

What are the limitations and key points to watch in the business model?

One limitation is transaction-based revenue’s sensitivity to market sentiment—lower activity directly impacts this category. Another is net interest’s reliance on interest rates and balance structure—macro rate changes alter its contribution. A third is subscription penetration, which has an upper limit; both benefit costs and customer acquisition costs should be monitored.

Key points to watch include: changes in the proportion of each revenue type, progress in PFOF regulatory discussions, crypto business share, and whether international expansion alters geographic revenue structure. These points aid in understanding mechanisms and do not constitute trading advice.

Summary

The essence of HOOD’s business model is its three revenue pillars—transaction-based revenue, net interest, and Gold subscription—combined with a multi-asset product matrix. Zero commission changes the explicit commission experience for users but does not eliminate revenue streams such as order routing, interest spread, and subscription fees. Understanding this structure, then comparing peer differentiation, regulatory constraints, and Gate trading processes, gives a more comprehensive view.

FAQ

How does Robinhood make money?

Primarily through transaction-based revenue, net interest revenue, and subscription fees like Robinhood Gold. Transaction-based revenue is tied to trading and order routing, net interest relates to client funds and lending, and subscription fees provide recurring income.

What is payment for order flow (PFOF)?

PFOF is compensation brokers receive when routing client orders to execution venues or market makers. It’s a market microstructure arrangement, not equivalent to users paying traditional stock commissions, and is subject to regulatory debate.

What is Robinhood Gold?

Robinhood Gold is a paid subscription service providing eligible users with a suite of value-added benefits, such as higher margin limits, data tools, and cash-related perks. Specific benefits are defined by product terms.

What does HOOD’s product matrix cover?

Typical offerings include stocks and ETFs, options, futures, event contracts, crypto trading and transfers, plus subscription and advisory products like Gold and Strategies. Some markets also feature bank credit partnership products.

Does zero commission mean Robinhood has no revenue?

No. Zero commission mainly refers to users paying zero or minimal explicit stock commissions; the company still recognizes revenue through transaction-based income, net interest, and subscriptions.