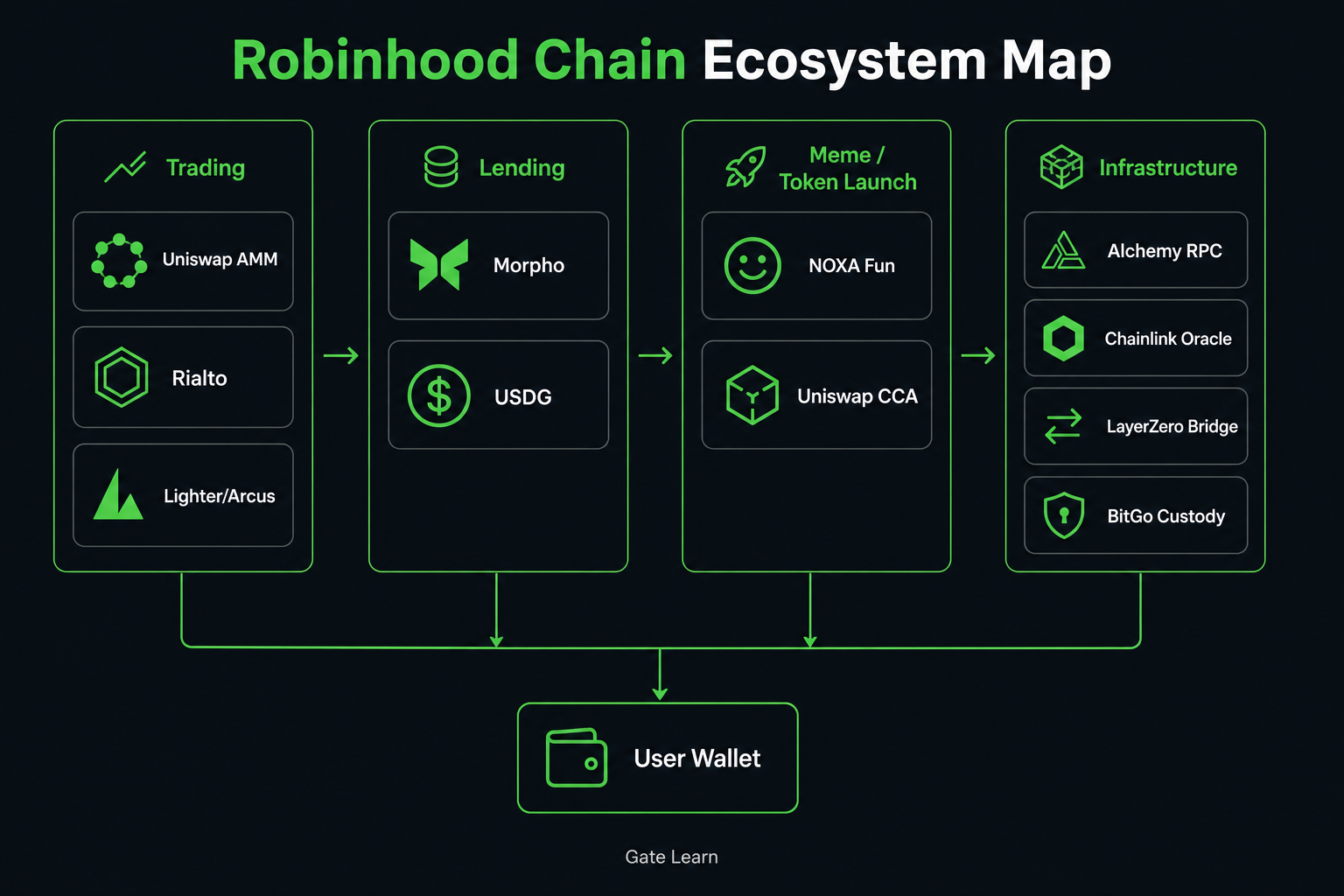

The Robinhood Chain ecosystem is structured into four primary layers: trading, lending, meme issuance, and infrastructure. At the top are DEXs, lending protocols, and launch platforms; the middle layer features stablecoins and liquidity tools; and the foundational layer consists of nodes, oracles, cross-chain, and custody components. Projects listed on the official ecosystem page and in developer documentation can generally be categorized within these four layers. When reviewing the ecosystem map, the emphasis should be on understanding which protocols serve which needs, rather than simply memorizing project names.

What Ecosystem Projects Are Available on Robinhood Chain?

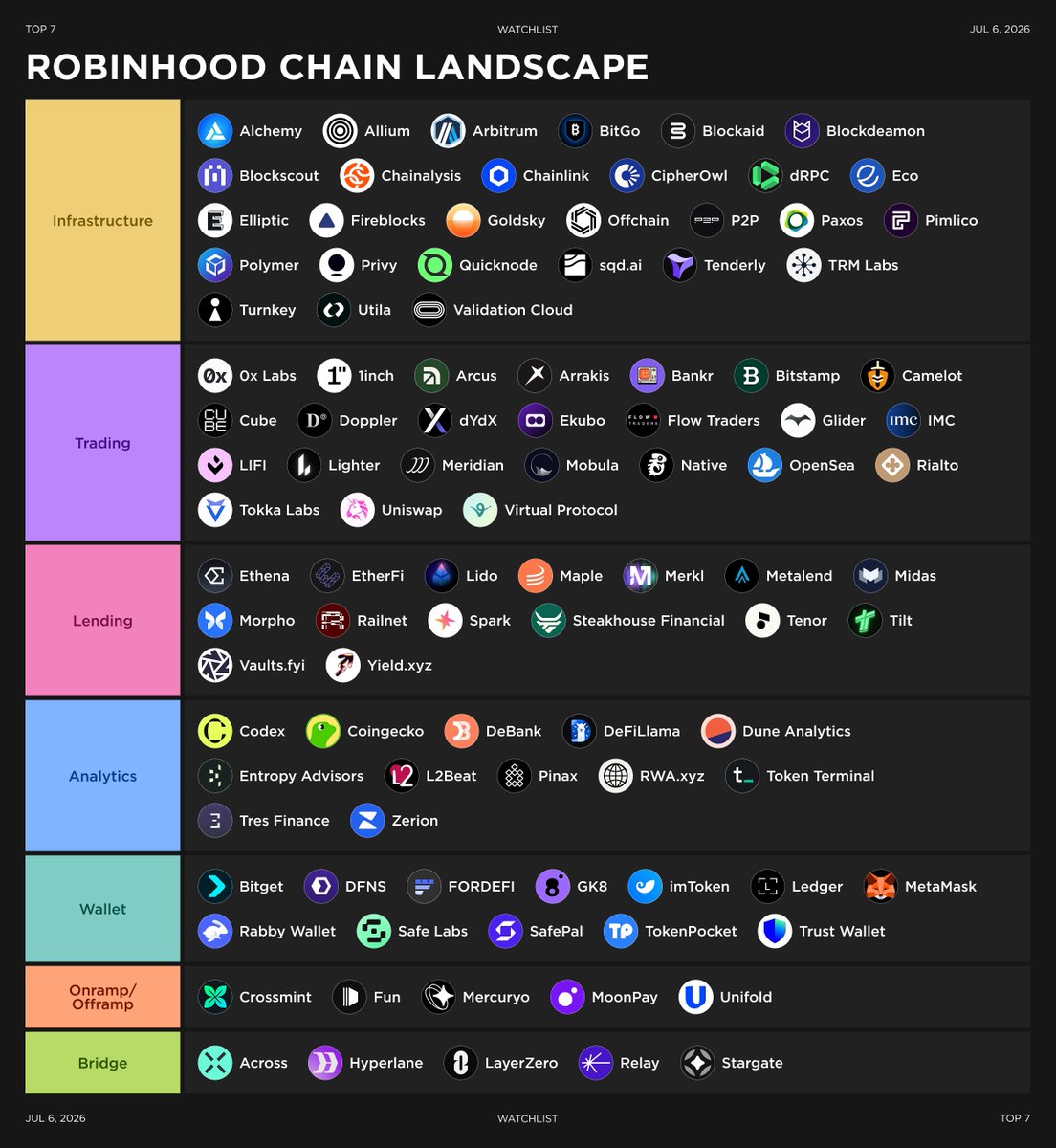

The public directory spans tracks such as trading, infrastructure, wallets, bridging, analytics, onramp/offramp, and lending. It’s important to note that a project’s inclusion does not imply platform endorsement or a guarantee of security.

Image source: top7ico

Image source: top7ico

When navigating this ecosystem map, the focus should be on understanding how demand flows: which protocols manage swaps and liquidity, which handle lending and liquidation, which are responsible for new token issuance, and which provide backend support such as nodes, oracles, custody, and risk management data. Breaking down these roles clarifies the ecosystem’s structure.

What Are the Main Destinations for Ecosystem Demand?

From the user journey perspective, demand on Robinhood Chain typically flows through four channels: starting with trading and liquidity, followed by lending and stablecoins, then meme issuance and cold starts, and finally, infrastructure that underpins the first three application types.

| Main Track |

Typical Label |

Primary Needs Addressed |

| Trading |

Trading |

Swaps, market making, perpetuals, and routing execution |

| Lending |

Lending |

Deposits, borrowing, collateralization, stablecoin pricing, and liquidation |

| Meme / Issuance |

Application Layer Issuance Tools |

New token creation, pricing, and liquidity bootstrapping |

| Infrastructure |

Infrastructure, Wallet, Bridge, Analytics |

Node access, oracles, cross-chain, custody, and on-chain data |

These four categories are interconnected. Trading builds liquidity; lending enables asset retention; issuance brings new assets to market; and infrastructure ensures upper-layer applications can reliably interact with the chain, provide price feeds, and support cross-chain functionality. As detailed in Account and Execution, a unified account experience often connects DEXs, lending protocols, and developer RPCs simultaneously.

| Project |

Track |

Description |

| Uniswap |

Trading |

Public DEX/AMM liquidity and token swaps |

| Morpho |

Lending |

Deposit, borrowing, collateralization, and liquidation rules |

| NOXA Fun |

Meme / Issuance |

New token creation and direct pool launches |

| Uniswap CCA |

Meme / Issuance |

On-chain auctions for pricing and liquidity bootstrapping |

| Alchemy |

Infrastructure |

RPC, Data API, and gasless transaction capabilities |

| Chainlink |

Infrastructure |

Price feeds and oracle support |

| LayerZero |

Infrastructure |

Cross-chain messaging and asset bridging |

This overview table provides a foundational understanding, with further breakdowns by track in the sections below.

Figure 1. The four core tracks of the Robinhood Chain ecosystem: trading, lending, meme issuance, and infrastructure.

Figure 1. The four core tracks of the Robinhood Chain ecosystem: trading, lending, meme issuance, and infrastructure.

Who Addresses Trading and Liquidity Needs?

On the trading side, Uniswap typically serves as the public DEX/AMM; Rialto and similar projects focus on PropAMM or spot routing; Lighter and Arcus are often associated with perpetuals and equity or commodity trading. The “trading entry” visible to users may involve multiple pools or execution paths behind the scenes.

Trading demand often consolidates around a few protocols at first, as new chains are initially validated by how smoothly swaps execute, how continuous pricing is, and whether liquidity pools are sufficiently deep.

| Function |

Representative Project (Documentation Context) |

User-Facing Role |

| Public DEX |

Uniswap |

Token swaps and public pool trading |

| Spot Routing / PropAMM |

Rialto, etc. |

Specialized spot execution paths |

| Perpetual Trading |

Lighter, Arcus, etc. |

Venues for leveraged or derivatives trading |

This table illustrates how trading demand is segmented: some protocols provide public liquidity, others optimize spot execution, and some channel demand toward perpetuals and derivatives. Focusing on a single product page can obscure this layered approach.

Who Addresses Lending and Stablecoin Needs?

Lending is primarily concerned with the retention of assets. Morpho delivers deposit, borrowing, collateralization, and liquidation rules; Paxos (USDG) and similar projects integrate USD stablecoins for pricing and settlement. Some lending or Earn products clarify that they operate on independent protocols, so product interfaces and on-chain protocol logic may be managed by different parties.

This layer is crucial, as liquidity generated by trading is more likely to be retained if it flows into lending, collateralization, and stablecoin markets.

| Function |

Representative Project (Documentation Context) |

User-Facing Role |

| Lending Primitive |

Morpho |

Deposit, borrowing, and liquidation rules |

| Stablecoin Infrastructure |

Paxos (USDG), etc. |

USD stablecoin and pricing foundation |

| Product Entry Layer |

Wallet / Earn Frontend |

User-friendly interface for on-chain lending |

The success of the lending layer often determines whether the Robinhood Chain ecosystem remains limited to high-frequency trading or evolves to support asset retention and longer usage cycles.

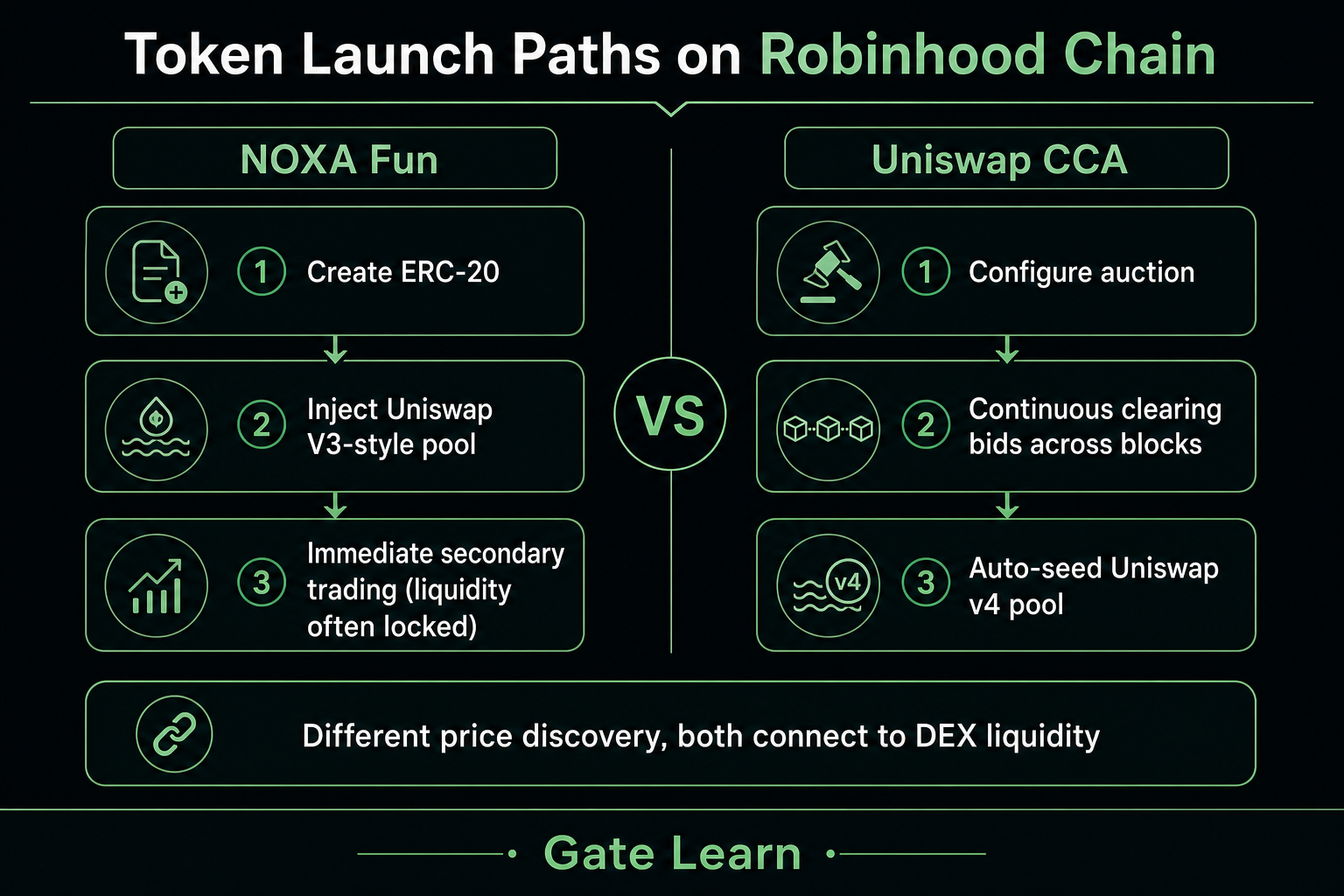

Meme and token issuance tools are typically the first to attract new attention on a chain. The core issue is how new tokens achieve price discovery and rapidly establish secondary liquidity. On Robinhood Chain, two common paths exist: direct pool launch via NOXA Fun and auction-based bootstrapping via Uniswap Continuous Clearing Auction (CCA).

NOXA Fun is an independent launchpad, not affiliated with Robinhood or equivalent to the Uniswap protocol. Its open mechanism often enables ERC-20 deployment and one-sided liquidity injection into a Uniswap V3-style pool in a single transaction, making the token tradable immediately. Many designs also lock liquidity, bypassing the need for a bonding curve before “graduating” to a DEX.

Uniswap CCA achieves price discovery and liquidity bootstrapping through on-chain auctions. Project teams set sale quantity, starting price, and duration; participants submit their maximum acceptable price and budget; the protocol clears continuously by block, with all winners in a block paying a unified clearing price. At auction close, funds are automatically injected into a Uniswap v4 pool at the discovered price. Users can typically browse, place bids, and claim via the Auctions section of the Uniswap Web App.

| Dimension |

NOXA Fun (Direct Pool Launch) |

Uniswap CCA (Auction Bootstrapping) |

| Positioning |

Independent launchpad |

Uniswap’s auction and liquidity bootstrapping tool |

| Price Discovery |

Direct trading in pool |

Multi-block continuous clearing, unified clearing price |

| Liquidity Connection |

Instant Uniswap V3-style pool integration |

Automatic injection into Uniswap v4 pool post-auction |

| Typical Use |

Rapid token launch and secondary trading |

Team-led fundraising and liquidity bootstrapping |

| Common Misconceptions |

Not a specific meme token |

Not a specific meme brand, but a general mechanism |

These two paths address different issuance needs. NOXA Fun is tailored for rapid token launches, while CCA focuses on price discovery followed by orderly liquidity integration. This aligns with the “open composability” discussed in the Base vs. Arbitrum comparison—the network’s EVM compatibility and open deployment enable third-party issuance tools to coexist with Uniswap’s liquidity layer.

Figure 2. Comparison of NOXA Fun direct pool launch and Uniswap CCA auction bootstrapping.

Figure 2. Comparison of NOXA Fun direct pool launch and Uniswap CCA auction bootstrapping.

Why Is Infrastructure the Foundation of Ecosystem Expansion?

Trading, lending, and issuance are application-layer functions; infrastructure is what ensures these applications operate reliably. Alchemy is frequently recommended for RPC and provides Data API and gasless transaction capabilities; Chainlink supplies price feeds and oracles; LayerZero manages cross-chain messaging and asset bridging; Fireblocks and BitGo provide institutional custody; Allium, CoinGecko, Zerion, and TRM Labs offer analytics, market data, wallet data, and compliance/risk tools, respectively.

Most users do not interact directly with these components, but their impact is evident in confirmation speed, price availability, cross-chain settlements, and anomaly tracking. For more details, refer to Security, Compliance, and Transparency.

How Can Regular Users Navigate the Ecosystem Map?

There is no single “correct” sequence, but following the official site’s categories helps ensure nothing is missed. Start by verifying wallets and onramp/offramp options to see how assets enter the network; then explore Trading, distinguishing between spot DEXs and perpetual/derivatives venues.

Next, review Lending: product interfaces and protocol-level rules for collateralization and liquidation may involve different providers. If interested in new token issuance, separately identify launchpads (such as NOXA Fun) and auction tools (such as Uniswap CCA), and always verify domains and contract addresses. Throughout, cross-check infrastructure: is RPC available, are oracles covering the relevant assets, and does bridging support your target network?

What Are the Risks and Limitations When Participating in Ecosystem Projects?

Risks primarily arise from third-party contracts, liquidity structure, and information asymmetry. Directory inclusion does not equate to a security rating; meme direct pool launches often involve high volatility and counterfeit asset risks; before participating in a CCA, understand bid locking, failed refunds, and fulfillment conditions; lending carries liquidation and oracle delay risks; cross-chain and custody introduce bridging and counterparty risks.

The directory itself has limitations: updates may lag, projects may rebrand or be discontinued, and the maturity of different tracks varies. It is best used as a navigational and organizational reference; relying on it as a security certification or yield indicator can lead to misinterpretation.

Summary

To understand Robinhood Chain’s ecosystem, focus on mapping out roles and responsibilities rather than memorizing project names. By categorizing projects into trading, lending, meme issuance, and infrastructure, most public directory entries fall into place: Uniswap and Morpho for swaps and lending; NOXA Fun and Uniswap CCA for different new token launch paths; and Alchemy, Chainlink, and LayerZero for node, price feed, and cross-chain support. Understanding these roles and risk boundaries is more valuable than simply knowing the names.

FAQ

What Ecosystem Projects Are Available on Robinhood Chain?

The public directory covers trading, lending, wallets, bridging, data, onramp/offramp, and infrastructure. Notable projects include Uniswap, Morpho, Alchemy, Chainlink, LayerZero, and on the issuance side, NOXA Fun and Uniswap CCA. Refer to the official ecosystem page and developer documentation for the most current list; inclusion does not imply endorsement.

What Categories Are Included in the Robinhood Chain Ecosystem?

Common categories include Trading, Infrastructure, Wallet, Bridge, Analytics, Onramp/Offramp, and Lending. For practical purposes, these can be summarized as trading, lending, meme issuance, and infrastructure. Categories are for organizational convenience and do not reflect maturity or security rankings.

What Is NOXA Fun? What Is Its Relationship to Robinhood Chain?

NOXA Fun is an independent third-party token launchpad that allows users to create tokens on Robinhood Chain and immediately connect liquidity to a Uniswap V3-style pool. NOXA Fun is not an official Robinhood product and is not equivalent to the Uniswap protocol. Always verify domain, contract, and liquidity lock rules before use.

What Is Uniswap CCA? How Should It Be Understood on Robinhood Chain?

CCA (Continuous Clearing Auction) is Uniswap’s on-chain auction tool for multi-block price discovery and subsequent liquidity connection to Uniswap v4. On Robinhood Chain, CCA functions as a token launch and fundraising tool, complementing spot DEXs rather than replacing them.

What’s the Difference Between NOXA Fun and Uniswap CCA?

NOXA Fun typically launches tokens directly into pools for trading; CCA completes price discovery via auction before integrating liquidity into v4 pools. The former is akin to a launchpad direct launch, the latter to protocol-driven fundraising and liquidity bootstrapping. Both serve new token onboarding, but differ in pricing mechanisms and liquidity integration timing.

Does Listing on the Official Site Mean Robinhood Endorsement?

No. The ecosystem page and documentation explicitly state that third-party inclusion does not constitute endorsement, partnership, or merchantability. Users must independently assess contract, interaction, and financial risks, and verify details using the project’s official materials.