Author: Yuan Chuan Investment Commentary

The recent Korean stock market performance is comparable to the “Ten Rings Roller Coaster” at Chimelong.

At the end of February, conflicts erupted between the US, Israel, and Iran. Amid expectations of a quick “Chuan Chuan Speed Pass Iran,” global stock markets withstood the first trading day on March 2nd. However, Korea’s stock market was closed all day due to a holiday.

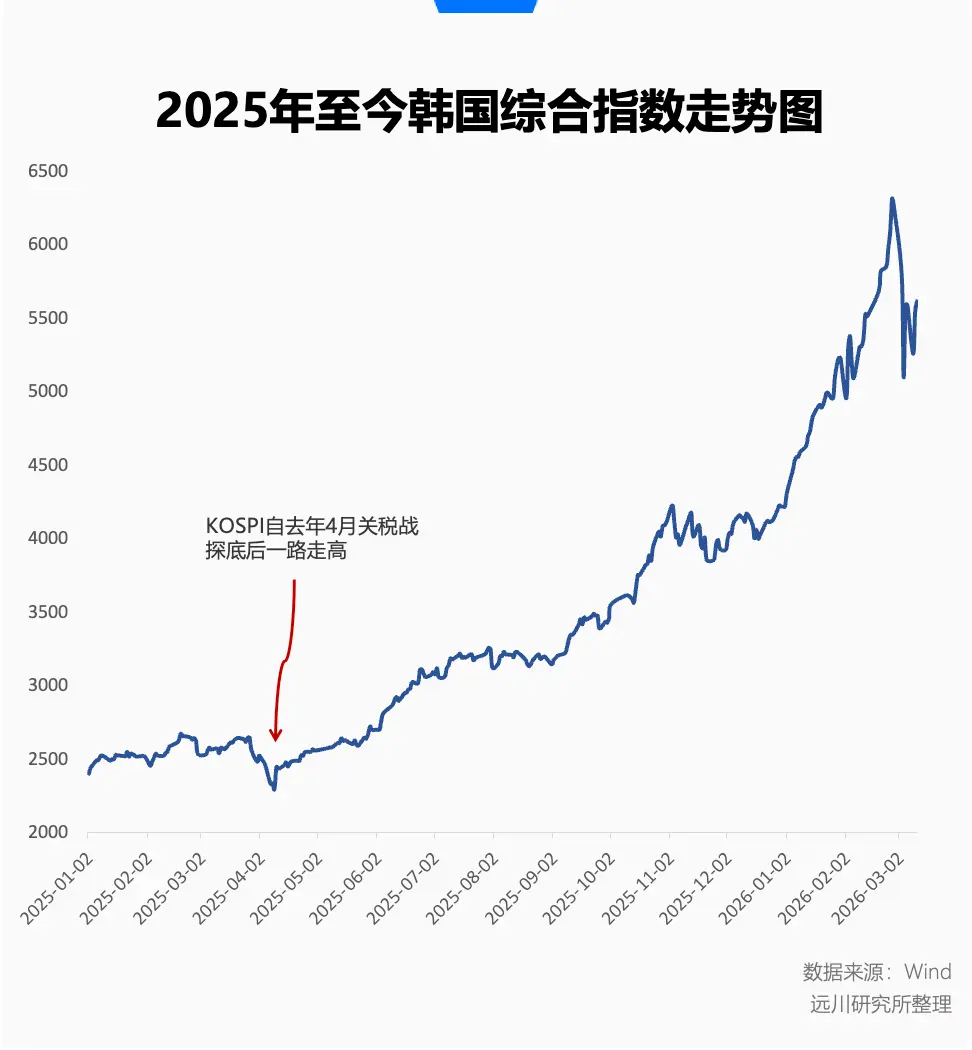

When it reopened on March 3rd, the expectation of a swift resolution in the Middle East had completely shifted. The Strait of Hormuz, under blockade, directly caused chaos in the global oil and gas markets. Meanwhile, the popular Korea Composite Index (KOSPI) has plunged into relentless decline since the beginning of 2026.

On March 3rd, the KOSPI temporarily hit the circuit breaker, ultimately falling more than 7%. The next day, it continued to hit the limit down, closing with a single-day drop of 12.06%, setting a record for the largest decline ever.

That evening, the Korea Financial Services Commission announced an immediate injection of 100 trillion won (about $680 billion USD) into the financial stability fund to stabilize the market. The following day, the KOSPI rebounded sharply by 9.63%.

But volatility did not stop there. This week, Korean stocks have continued to swing wildly between extremes, with a nearly 6% decline on Monday and a 5.35% rise on Tuesday. All while investors who hoped for a violent rebound are once again experiencing the fundamental lesson of “volatility decay.”

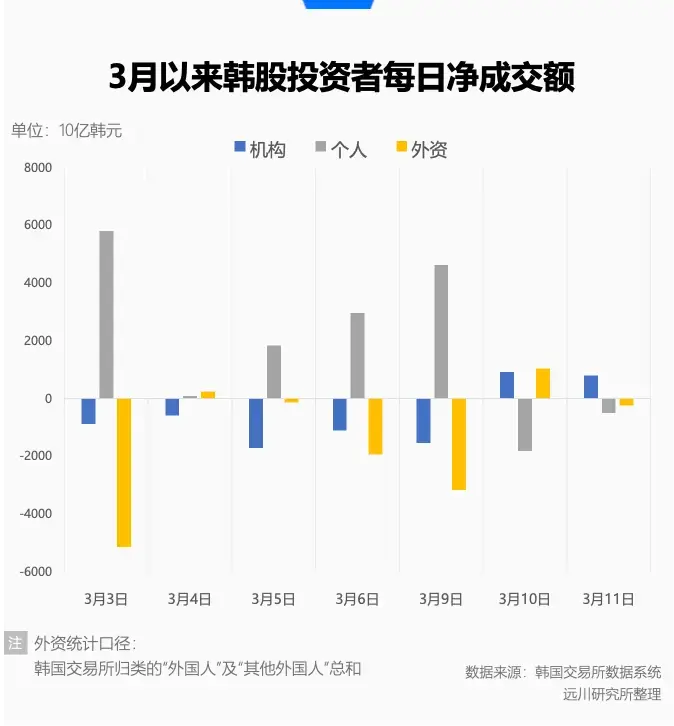

Meanwhile, statistics from the Korea Exchange reveal an interesting phenomenon. Since March, domestic retail investors have been net buyers, while foreign investors have been net sellers. This seems to echo the 2020 pandemic storm, where greater volatility led to increased foreign selling and retail buying.

Before these days of sharp rises and falls, the Korean stock market experienced an unprecedented upward cycle. From 2025 to late February 2026, the KOSPI surged over 160%, making it the MVP of global markets. During this “bullish” period, the KOSPI doubled from 3,000 to 6,000 points in less time than the fastest record in Nasdaq history[10].

This explosive growth, combined with extreme fluctuations during crises, creates a complex picture of the Korean stock market.

The Night Before the Black Swan

From the curve, it’s clear that the upward trend in Korean stocks actually began after the tariff war bottomed out in April last year.

At that time, global markets trembled amid Trump’s latest tariff trade, and after a cumulative drop of over 7% in early April, the KOSPI started climbing out of the trough. Even brief corrections in November were seen as signals of “reverse gear” by enthusiastic market sentiment.

The revived enthusiasm for Korea intensified after the start of 2026. The KOSPI nearly achieved a year’s worth of KPI in January, and despite increased volatility in February, the upward momentum accelerated.

On the first trading day of February, the KOSPI retraced 5.26%, the largest pullback during this rally, but the external environment was still relatively stable. This “stress test” was quickly recovered amid oscillations. On February 25th, the KOSPI first crossed 6,000 points, and on the last trading day of February, it hit a high of 6,347.41 points intraday, then retreated, ending the month down 1%.

Rapid gains are not without reason, aligning with the principle that higher concentration and elasticity lead to greater volatility.

Looking at the index composition, although officially called the Korea Composite Stock Price Index, it is essentially a highly concentrated “race track gambler.” The market value of the two major memory chip giants, Samsung and SK Hynix, accounts for one-third of the Korean stock market. The KOSPI’s rise heavily depends on these two core stocks.

Before March, the KOSPI was a pure AI mapping, with Samsung and SK Hynix holding the key to the AI era like new oil. Whether it’s the soaring demand for high-end products like HBM (High Bandwidth Memory) needed for AI large models, or the supply contraction of DRAM/NAND due to capacity constraints in traditional consumer electronics, storage has become the most popular wealth code of 2026.

From late 2025 to early 2026, Samsung and Hynix mainly announced price hikes—DRAM/NAND prices were sharply increased for three consecutive quarters starting in Q3 2025; HBM4, still ramping up production, became a seller’s market. By 2026, capacity was already divided among AI giants, and even the wealthiest could only wait for the 2027 supply.

However, when the world realized that the unstable Gulf would cut off stable oil supplies, the grand narrative of the future was quickly overshadowed by immediate energy shortages. Especially for Korea, heavily dependent on Middle Eastern oil and gas, the story shifted overnight from “AI mapping king” with FOMO to “victim of high oil prices” with HALO anxiety.

In the first two trading days of March, Samsung and Hynix fell about 10% for two consecutive days.

In fact, before this “black swan,” both domestic Korean funds and foreign investors had already diverged. In February, the average daily trading volume of Korean stocks reached 32.23 trillion won (about 1,492 billion RMB), up 19% from January, setting new records for both index and trading volume.

From a technical analysis perspective, this volume surge and new high are classic “signal exchange” indicators.

Since May last year, foreign investors have maintained a net buy stance overall, but after the KOSPI hit 6,000 points, they began to sell in bulk. In February, foreign net sales hit a record high of 21.1 trillion won (about 998 billion RMB). On February 27th, when the KOSPI hit a new intraday high, foreign net selling was 7 trillion won (about 324 billion RMB).

However, these profits may not have anticipated that the structurally imbalanced Korean stock market would pay such a heavy price due to the “epic fury” and “real commitments” from the distant Middle East.

The Self-Help of the Non-Expert

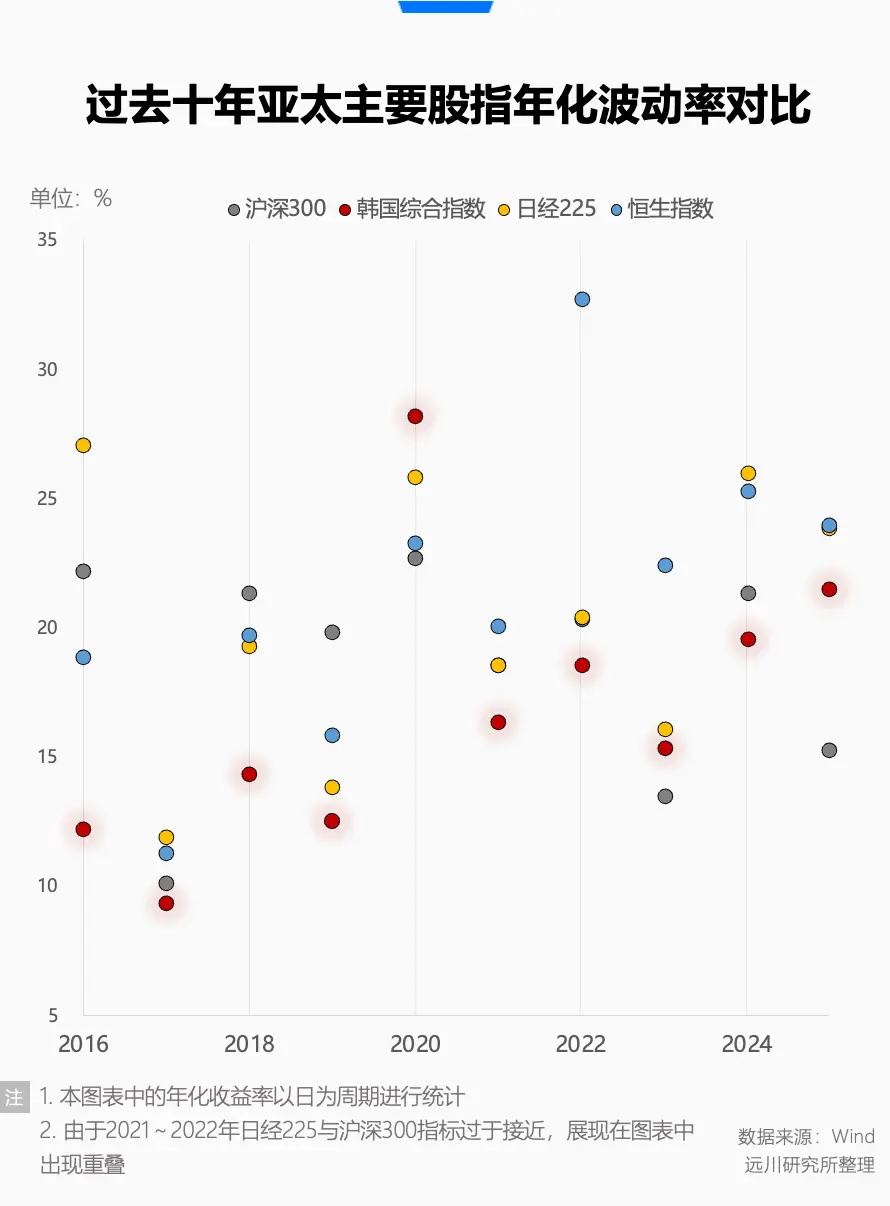

Such dramatic rises and falls naturally raise questions about the volatility of the Korean stock market.

In fact, over the past decade, among the four major Asia-Pacific indices (CSI 300, Hang Seng Index, Nikkei 225, and Korea Composite Index), the CSI 300 has an annualized volatility of 18.12%, KOSPI 18.90%, and Nikkei 20.50%, ranking second. The Hang Seng Index leads with 21.79%, which is not surprising.

Before 2025, the KOSPI only experienced a major fluctuation once in 2020, with a storyline similar to March this year—Korean stocks were hammered down during heavy foreign selling, then retail investors entered to buy the dip, pushing the market higher.

For years, Korea’s low volatility was coupled with the awkward “Korean discount.”

Over the past decade, the overall market price-to-book ratio hovered around 1, occasionally rising slightly but then returning to low levels. Only after the spectacular rally since last year did it reach a high of 2 in February this year.

Even though Korea’s stock market is generally less attractive, with only Samsung and Hynix being market favorites, Taiwan’s semiconductor index typically has a P/B ratio around 2.4.

The “Korean discount” can also be seen as a collective negative assessment by global investors. The problem isn’t just the index’s skewed focus but also the governance models of large listed companies, which often don’t meet modern investor expectations.

Both Samsung and SK are typical family-controlled chaebols, with opaque governance. Many times, they suppress stock prices, avoid dividends, or use cash for blind diversification to evade high inheritance and dividend taxes. All these factors have made the Korean stock market notorious for being “stingy” to small shareholders.

Recent Korean presidents have all made “solving the Korean discount” a key agenda.

Former President Moon Jae-in encouraged institutional investors like the National Pension Service (NPS) to actively participate in corporate governance, attempting to address low valuations by limiting chaebol cross-shareholdings and strengthening minority shareholder rights.

Predecessor Yoon Suk-yeol launched a “Corporate Value Enhancement Plan,” aiming to revitalize the market through tax cuts, voluntary disclosure, and increased dividends. But he resigned amid political turmoil in April 2025, and the “Korean T-Estimate” faded away.

In June 2025, current President Lee Jae-myung took office, calling for sweeping reforms of the capital market, including a campaign slogan to push the KOSPI to 5,000 points.

As a former seasoned retail investor (with losses), Lee Jae-myung has long been frustrated by the unfair dealings of major shareholders, which he believes exacerbate ordinary investors’ losses.

After taking office, he implemented a series of reforms, including but not limited to: mandating the cancellation of controlling chaebol’s treasury stocks; strengthening board accountability; reforming dividend taxes to encourage payouts; and promoting wealth transfer from real estate speculation to financial assets.

Lee often emphasizes his own background as a retail investor and claims that once his political career ends, he will return to stock trading[11].

Whether driven by top-down strategic needs or personal experience, Lee’s enthusiasm for reform has helped him fulfill his campaign promise to push the KOSPI above 5,000 points. Even considering recent volatility, the index has risen over 100% within less than a year of his tenure.

Before the Gulf crisis, Lee’s market reforms received considerable attention. Bloomberg published a headline titled “How the Korean President is Making Korea’s Stock Market the Best in the World,” calling him a hero among Korea’s 14 million retail investors[11].

Of course, this article was published on February 22, 2026, when ships still navigated the Strait of Hormuz normally, investors debated the future of AI in Citrini’s “2028 Smart Crisis,” and oil prices hovered above $60, calm and steady.

Epilogue

If Lee Jae-myung’s reforms aimed to address “rules” and “distribution,” trying to fix long-term low valuations, then the Middle Eastern conflict instantly shattered the profit expectations as the denominator, pulling market focus sharply back to short-term inflation and survival.

This split reveals a harsh reality: reform-driven bull markets are built on relatively stable global macro assumptions. When the Gulf conflict’s timeline extends, it exposes Korea’s vulnerabilities as resource-scarce export-dependent economy with over-concentrated industries.

In an open market, funds flowing in due to industry advantages or reform expectations can reverse out during crises. Especially when global risk aversion spikes and foreign investors hold large profits, liquid assets with the highest gains are naturally the first to be sold off.

To some extent, this is an unavoidable fluctuation in a highly open market and a new challenge in expectations management.

Just look at the neighboring Hong Kong stocks—despite a diverse industry structure and relatively advanced corporate governance—when turned into a “cash machine,” their declines are just as swift and ruthless.