The Strait of Hormuz is nearly paralyzed, and oil-producing countries in the Persian Gulf are forced to cut production. International oil prices once surged past $110 per barrel, reaching a two-year high. JPMorgan warns that the market is shifting from “geopolitical risk pricing” to “actual supply disruptions,” and global inflation is heating up again.

(Background: Trump “temporarily not seizing Iranian oil”: further blockade of the Strait of Hormuz would be 20 times more damaging; EU releases oil reserves in response)

(Additional context: Iran threatens to bomb U.S. naval fleets and block the Strait of Hormuz. Trump: Retaliation would only invite more severe attacks.)

The Iran conflict continues to escalate, further worsening the situation in the Persian Gulf. The United Arab Emirates and Kuwait announced last weekend that they are reducing oil production due to the near-complete closure of the Strait of Hormuz, causing their oil storage tanks to fill rapidly.

Large amounts of oil stranded, Persian Gulf exports halted

Because Iran has threatened to attack ships passing through the Strait of Hormuz, major oil producers in the Persian Gulf—Saudi Arabia, the UAE, Iraq, and Kuwait—are forced to suspend shipments to global refineries.

UAE’s state-owned Abu Dhabi National Oil Company (ADNOC) said it is reducing offshore oil field output; Kuwait Petroleum Corporation has also cut back on oil field and refinery production. Sources say Kuwait, which produces about 2.56 million barrels daily, has cut 100,000 barrels per day since the 7th, with plans to increase cuts to nearly 300,000 barrels on the 8th.

Additionally, Iraq has begun reducing output as its storage tanks are full, and Saudi Arabia has shut down its largest refinery. Qatar, after drone attacks, has closed its biggest liquefied natural gas export plant.

Oil prices briefly soared past $110

The blockade of the Strait of Hormuz pushed international oil prices above $110 per barrel on the 9th, the highest in over two years. JPMorgan’s report states:

The market is shifting focus from purely geopolitical risks to actual operational disruptions, as refinery shutdowns and export restrictions begin to impair crude processing and regional supply.

Earlier, G7 issued a statement saying they are prepared to take necessary measures to support global energy supplies, including releasing oil reserves, though no decision has been made yet. An official familiar with G7 finance ministers’ discussions said:

There is a general consensus on this. It’s not opposition; it’s a matter of timing, and more analysis is needed.

Analysts warn that the Iran conflict could lead to high oil prices for consumers and businesses worldwide for weeks or even months. Even if the conflict ends quickly, suppliers will still face damaged oil facilities, logistical disruptions, and rising transportation risks, posing a threat to the global economy.

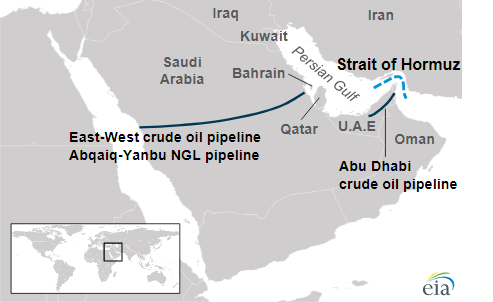

Three pipelines could theoretically save 30%

You might wonder, if the sea route is blocked, are there alternative options? The good news is that infrastructure bypassing the Strait of Hormuz does exist.

Saudi Arabia’s East-West Pipeline runs from the Abqaiq processing center on the Persian Gulf coast to Yanbu on the Red Sea coast, spanning 1,200 km. Designed capacity is 5 million barrels per day, but Saudi Aramco claims it has expanded to 7 million barrels.

Currently, actual usage is about 2 million barrels daily, leaving 3 to 5 million barrels of theoretical spare capacity. On March 6, Saudi Arabia announced it would redirect several million barrels of oil to Red Sea exports.

(Left) East-West Pipeline (Right) Abu Dhabi Crude Oil Pipeline

UAE’s ADCOP pipeline connects the inland Habshan oil field to Fujairah port on the Oman Sea, stretching 400 km with a capacity of 1.8 million barrels per day. Current exports are about 1.1 million barrels, with roughly 700,000 barrels of spare capacity.

Iran’s Goreh-Jask pipeline links to the Jask port on the Oman Sea, with effective capacity of only 300,000 barrels per day. Under current circumstances, Iran’s own exports are also constrained by sanctions and military pressure.

In total, these three pipelines offer a theoretical spare capacity of about 3.7 to 5.7 million barrels. That sounds substantial, but the daily throughput of the Strait of Hormuz is 20 million barrels, meaning these alternatives can only cover roughly 25% to 35%.

Jebel Ali port isn’t designed for this scenario

Numbers on capacity are one thing; logistics are another.

Jebel Ali has never been Saudi Arabia’s main export port. Its docks, storage tanks, and tanker scheduling are built with backup in mind. Suddenly shifting hundreds of thousands of barrels daily from the east coast to the west coast creates bottlenecks—not in pipelines, but in port capacity and how quickly ships can be loaded.

According to The National, under high-pressure operation, Jebel Ali’s loading efficiency might only reach 60% of pipeline capacity.

Worse, the Red Sea itself is also unstable. Although recent threats from the Houthis have eased, they have not been eliminated. Rerouting around the Hormuz Strait to another area with missile risks means insurance companies probably won’t find this business very attractive.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.