Image source: Ember Post

Image source: Ember Post

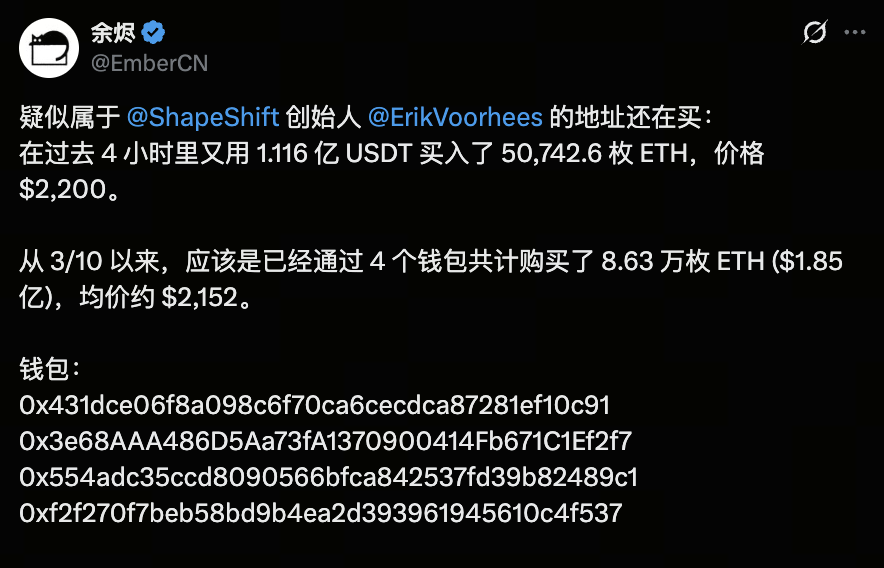

On March 19, 2026, a significant on-chain purchase once again captured market attention. According to on-chain analyst EmberCN, an address suspected to be associated with Erik Voorhees acquired roughly 50,742 Ethereum in the past four hours, totaling about $112 million at an average price of $2,200. Since March 10, this entity has accumulated approximately 86,300 ETH, with a total value of about $185 million and an average cost of $2,152.

This sustained capital activity has established a clear “capital cost band” for ETH in the $2,100–$2,200 range, reigniting debate about Ethereum’s medium-term outlook: Now that BTC has completed a dominant rally, is ETH entering a new phase of repricing?

Image source: Gate Market Page

Image source: Gate Market Page

During the last cycle, Bitcoin surged past $126,000, and while Ethereum also rallied, its overall performance clearly lagged. The ETH/BTC ratio remains near historical lows, reflecting ongoing capital preference for BTC. This divergence is not merely about price movements—it’s the result of capital structure, product channels, and market narrative working together.

In short, ETH’s relative weakness does not necessarily signal diminished long-term value. More likely, it remains in a “delayed repricing” phase, which is precisely why the market is once again focused on its potential to catch up.

Why Does BTC Lead While ETH Is Prone to Lag?

The defining change in this cycle is that institutional capital poured into BTC first. Reuters reported that in October 2025, global crypto ETFs saw a record $5.95 billion in weekly inflows, with Bitcoin attracting $3.55 billion and ETH $1.48 billion. Although ETH drew substantial capital, the preference for BTC was clear. For large investors, BTC’s “digital gold” narrative is more straightforward, regulatory hurdles are lower, and productization is more transparent.

This creates a classic capital hierarchy: BTC first absorbs the most certain and conservative allocations. Only when BTC enters high-level consolidation and risk appetite rises does capital begin to flow into ETH. Thus, ETH underperforming BTC is not due to a lack of value, but because it typically follows BTC in the capital allocation order—a recurring pattern in past cycles.

Ethereum’s Challenge: Not “No Ecosystem,” but Weaker Value Capture

Technically, Ethereum remains one of the crypto market’s most critical settlement and security layers. The official Ethereum documentation notes that Layer 2 solutions process transactions off the mainnet, relying on Ethereum Mainnet as the settlement layer. Rollups compress transaction data and submit it on-chain, inheriting security and lowering costs. While this architecture accelerates scaling and reduces fees, it also means that many fees that once accrued directly to the mainnet are now diverted to L2.

This is ETH’s core dilemma: its ecosystem remains strong, but its ability to directly capture value from on-chain activity is no longer as robust. Previously, more users and higher gas fees reinforced ETH’s narrative. Now, as more transactions shift to L2, Ethereum’s network growth and ETH token price are no longer naturally synchronized. Official sources confirm that Ethereum’s Layer 2 design intentionally shifts transactions off the mainnet to boost throughput and lower costs.

The result: ETH remains a foundational infrastructure asset, but can no longer directly convert all ecosystem growth into strong token price appreciation as before. The market is now asking: if the mainnet no longer captures sufficient fee revenue, what should anchor ETH’s valuation?

Does ETH Still Have Fundamental Support? Yes, but the Logic Has Changed

Image source: Etherscan Gas Tracker

Image source: Etherscan Gas Tracker

If we focus only on “mainnet fee revenue,” ETH’s narrative does appear weaker than before, but that doesn’t mean it has lost long-term support. Ethereum’s PoS mechanism still requires validators to stake ETH to secure the network, and staking provides rewards. Official documentation emphasizes that staking is not only a source of yield but also integral to network security. In other words, ETH now serves as both an asset and collateral for network security—unlike a pure payment token.

In addition, Ethereum’s recent technical roadmap continues to reinforce its “settlement layer” role. The Pectra upgrade, as outlined in the official roadmap, advances staking-related optimizations, showing that Ethereum is not regressing but evolving toward a more efficient security and settlement system. Over the long term, these upgrades are not meant to trigger immediate price surges for ETH, but to stabilize its core demand, make staking more flexible, and clarify its asset attributes.

Therefore, the core question for ETH has never been “does it have fundamentals,” but rather “how does the market choose to value it.” BTC is valued more like a macro asset, while ETH is a composite asset with infrastructure, yield, and ecosystem collateral characteristics. The upside of a composite asset is a higher potential ceiling; the downside is that the market often struggles to assign a unified, rapid valuation.

Why Does the Market Keep Asking If ETH Will Catch Up?

Because ETH’s historical pattern is “later, but with greater elasticity.” When capital concentrates in BTC, ETH’s performance is often mediocre; but when BTC trades sideways or its rally slows, the market seeks higher-beta assets, and ETH is typically among the first to attract inflows. This logic is structural, not merely emotional.

Recently, notable on-chain signals have emerged. Data on X indicates that a wallet suspected to be linked to ShapeShift founder Erik Voorhees has been accumulating ETH in recent days, totaling nearly 86,300 ETH at an average cost of $2,152. While this does not guarantee a market reversal, it does suggest that capital with a deeper understanding of crypto structures is starting to reallocate into ETH.

The significance of these actions lies in their establishment of a “mid-term cost zone”—not a one-off emotional trade, but a strategic positioning. In other words, the market may be forming a new valuation anchor: if ETH continues to be accumulated within a certain range, its subsequent price performance will depend not only on BTC, but also on ETH’s ability to turn this cost base into support.

When Can ETH Truly Strengthen?

ETH typically needs three conditions to rally meaningfully: First, BTC’s upward momentum must slow, so capital is no longer solely focused on the most certain asset. Second, ETH itself must see clear capital inflows or improved on-chain activity. Third, the market must once again embrace a composite valuation framework—viewing ETH as not just mainnet gas, but as settlement layer, staking asset, and ecosystem foundation. If only one condition is met, ETH may merely rebound; if all three align, a true catch-up cycle is more likely.

Based on current public information, the most realistic assessment is not that “ETH has fallen behind with no chance,” but that “ETH has yet to enter its main repricing phase.” On March 17, 2026, Citigroup lowered its 12-month targets for BTC and ETH, noting that stalled US crypto legislation has dampened institutional adoption and ETF demand, and also highlighted Ether’s particular sensitivity to user activity metrics. This view aligns with market trends: ETH is not lacking a narrative, but it still lacks strong enough capital and policy catalysts.

Conclusion

If the relationship between ETH and BTC is a capital race, BTC is the “first-choice asset” for institutions and macro funds, while ETH is a more complex, but also more flexible, follow-up asset. ETH’s persistent underperformance is not due to weak fundamentals, but because its value capture, product adoption, and narrative priorities are all more difficult for the market to price quickly at the start of a bull cycle.

Therefore, ETH’s future upside is not about “whether it has value,” but about “when the market is willing to assign it a higher valuation multiple.” If capital starts to flow out of BTC and ETH’s on-chain activity, staking yields, and settlement layer narrative are all strengthened, ETH could make up for its earlier underperformance in a much more aggressive fashion. (This article does not constitute investment advice. Please trade cautiously and be mindful of risks.)