SEC Approves Nasdaq Pilot: Tokenized Securities Enter Regulatory Implementation Phase

In March 2026, the US Securities and Exchange Commission (SEC) formally approved a rule change for Nasdaq, enabling the exchange to launch a pilot for “Tokenized Securities” trading within its system. This marks the first time blockchain technology has been integrated into mainstream securities market infrastructure in a fully compliant manner. From an industry perspective, tokenization has progressed from a conceptual narrative to regulatory implementation, and Real World Assets (RWA) are now gaining substantive recognition from regulators.

What Are Tokenized Securities? Essential Analysis

Tokenized securities are not a new asset class. Instead, they represent traditional securities expressed through blockchain technology. At their core: Tokenized Securities = Securities + Blockchain Representation Layer. Under this framework, the legal nature of the asset remains unchanged—still regulated under securities law—while only the recordkeeping and circulation methods change:

- Legal attributes unchanged: still classified as securities and subject to regulatory oversight

- Technical structure shift: from centralized databases to distributed ledgers

- Trading method upgrade: tokens are introduced as carriers for circulation and settlement

This structure ensures that tokenization does not bypass regulation, but rather becomes part of the existing financial system.

Two Core Divergences: Native vs. Wrapped Models

Tokenized securities development currently follows two main models, which will directly shape the industry’s future:

- Native issuance: Enterprises directly issue securities on the blockchain, enabling on-chain registration, trading, and settlement of equity.

- Wrapped issuance: Custodians hold traditional securities and map them as tokens, essentially relying on centralized institutions.

Issuers may also differ—first-party or third-party—where third-party issuance can introduce unequal rights.

Overall, the current Nasdaq pilot aligns more closely with the Wrapped model, representing a hybrid of traditional finance and blockchain.

SEC’s Three Regulatory Bottom Lines: Innovation Must Not Compromise Investor Protection

While blockchain technology is being introduced, the SEC insists that core capital market rules remain inviolable. Its regulatory bottom lines are:

- Complete information disclosure: Investors must clearly understand the voting rights, dividend rights, and legal status tied to their assets, preventing any disconnect between tokens and equity.

- Regulated intermediaries: Issuers, trading, and settlement entities must be included in the regulatory system, meaning fully anonymous DeFi models are unlikely to enter the securities market.

- Best execution principle: Markets must ensure that investors receive optimal pricing, preventing fragmented liquidity from impacting trade quality.

These principles show that tokenization’s path is “innovation within the rules,” not “circumventing the rules.”

Core Advantages of Tokenized Securities: Efficiency, Transparency, and Liquidity

From a market structure perspective, tokenized securities deliver significant efficiency gains—the primary reason for their adoption.

- Atomic settlement enables simultaneous delivery of assets and funds, shifting settlement cycles from T+1 to real time and reducing counterparty risk.

- Blockchain offers greater transparency, allowing real-time shareholder structure queries and reducing information asymmetry.

- Tokenization supports 24/7 trading, integrating global liquidity and improving asset pricing efficiency.

By streamlining clearing and custody, overall market costs may decrease. The core advantages can be summarized as:

- Enhanced settlement efficiency and capital utilization

- Improved market transparency and verifiability

- Around-the-clock trading and global liquidity integration

- Lower intermediary costs and reduced system complexity

Real-World Challenges and Potential Risks: Regulatory and Decentralization Conflicts

Despite its promise, tokenized securities face several challenges:

- Atomic settlement reduces risk but also diminishes the net settlement advantages of traditional finance, increasing capital usage costs.

- Blockchain’s openness conflicts with securities regulatory requirements, especially regarding KYC and anonymous transactions.

- On-chain markets lack mature stabilization mechanisms—such as circuit breakers and market-making systems—which may amplify volatility during extreme conditions.

- In the Wrapped model, token holders’ legal rights are still not fully defined.

Overall risks include:

- Reduced capital efficiency and liquidity pressures

- Structural contradictions between decentralization and regulatory requirements

- Underdeveloped market stabilization mechanisms

- Complex legal and ownership definitions

Far-Reaching Impact on RWA and the Crypto Market

The SEC’s approval of the tokenized securities pilot affects both traditional finance and the crypto market in profound ways:

- It affirms the long-term value of the RWA sector, moving tokenization from narrative to institutional development.

- It promotes integration between traditional finance and blockchain ecosystems, with potential emergence of on-chain securities, on-chain ETFs, and cross-market liquidity integration.

- It creates new pathways for institutional capital, enabling gradual exposure to blockchain infrastructure via familiar securities assets.

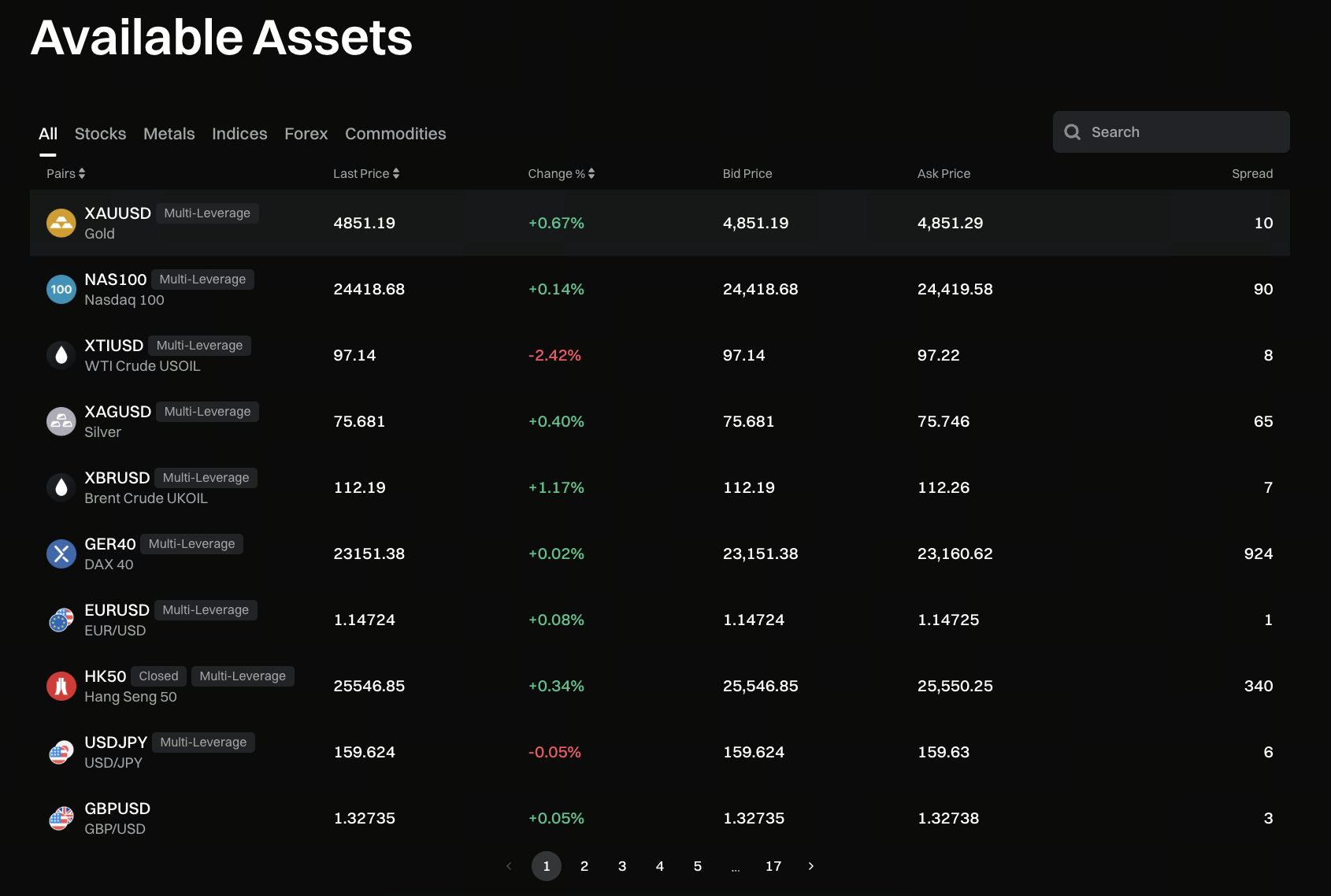

Image source: Gate TradFi page

Image source: Gate TradFi page

The launch of Gate TradFi also demonstrates that the boundaries between traditional finance and crypto trading are becoming increasingly integrated. According to Gate, users can trade TradFi assets—including gold, forex, and indices—with a single account, accessing both crypto and traditional financial markets on one platform. The significance of these products lies not only in expanding asset classes, but also in connecting “on-chain assetization” and “unified trading entry,” turning tokenization from a concept into accessible trading scenarios.

Future Trends: How Will Tokenization Reshape Capital Markets?

From both policy and technical perspectives, tokenization will advance gradually. In the short term, markets will maintain a hybrid model of traditional financial infrastructure and blockchain technology, rather than adopting a fully decentralized structure. In the long term, as regulation adapts, the market may evolve in the following directions:

- Gradual emergence of native on-chain securities

- Globalized 24/7 trading becomes standard

- Clearing and custody systems are compressed or restructured

- Deep integration between capital markets and blockchain networks

Conclusion: Tokenization Is the Evolution of the Financial System, Not Its Disruption

The SEC’s approval of Nasdaq’s tokenized securities pilot reflects traditional finance proactively adopting blockchain technology, not being disrupted by it. The core value of tokenization lies in greater efficiency, transparency, and global liquidity—not in replacing the existing system. As this trend continues, a more blockchain-integrated, real-time, and global capital market structure is gradually emerging.