Latest Signal: Wall Street’s Entry Shifts from “Allocation” to “Productization”

In the past two years, “institutional entry” was often synonymous with “buying Spot ETFs.” The latest developments, however, mark a new phase: Wall Street is moving from passive allocation to active product creation.

On April 14, 2026, Goldman Sachs filed registration documents for the Goldman Sachs Bitcoin Premium Income ETF, essentially converting Bitcoin volatility into distributable Return. Meanwhile, Morgan Stanley is driving Bitcoin allocation through proprietary products and its wealth advisor network, expanding capital flows from trading platforms to traditional asset management systems.

This signals a pivotal shift:

Crypto Assets are no longer just “tradable instruments”—they’re being engineered as “marketable products.” As the industry enters this product industrialization stage, capital structure will transition from short-term trading-driven to medium- and long-term Asset Allocation-driven flows.

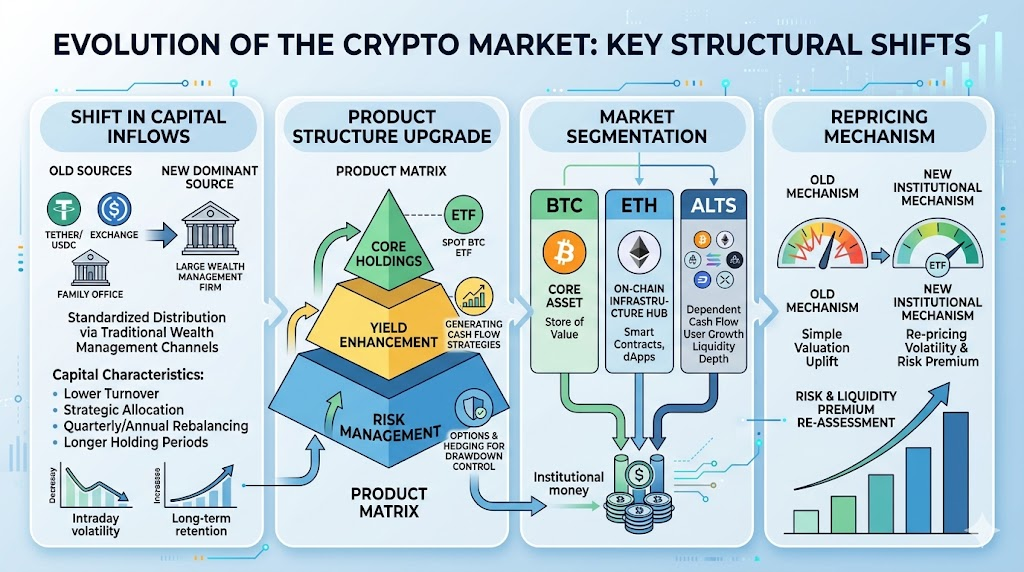

Capital Entry Restructuring: From On-Chain Native Liquidity to Traditional Asset Management Distribution

Historically, capital entered the crypto market through three main channels:

- Stablecoin issuance and on-chain migration

- Exchange Spot and Futures funds

- Limited direct investments from family offices and high-net-worth individuals

Now, a fourth—and potentially the largest—entry has emerged:

Standardized distribution via traditional wealth management channels.

This evolution brings three core consequences:

- Capital profile: shifting from high-turnover, sentiment-driven funds to medium- and low-turnover, strategy-driven allocation.

- Capital rhythm: moving from “news-driven intraday volatility” to “quarterly and annual rebalancing.”

- Capital stability: once channel funds clear investment committee and compliance reviews, their retention cycles are typically much longer.

In summary, the market is no longer solely reliant on “new narratives to attract new users,” but is leveraging “new distribution channels to expand AUM.”

Product Structure Evolution: Spot ETFs, Yield-Enhancing ETFs, and Derivative Synergy

The current focus isn’t on a single ETF, but on the emergence of a product matrix.

Structurally, Wall Street is building a three-tier system: “core positions + yield enhancement + risk hedging”:

- Core positions: Spot BTC ETFs as the foundational allocation to meet directional demand

- Yield enhancement: strategies like covered calls convert volatility into cash flow, appealing to risk-averse capital

- Risk management: options, structured notes, and cross-asset hedging tools control portfolio drawdown

This will reshape participant behavior:

- In bull phases, yield-enhancing products may “sell upside potential,” dampening extreme short-squeeze moves.

- During consolidation, option premiums and dividend narratives can increase capital retention.

- In downturns, institutional rebalancing may amplify correlations, driving synchronized de-risking.

Thus, the key market variable is no longer just “is there new capital,” but “in what product form does new capital enter?”

Deepening Market Stratification: BTC as Core, ETH as Hub, Altcoins as High Beta

Wall Street capital typically prioritizes high-liquidity, high-compliance Assets, further stratifying the crypto market:

- First tier: BTC as the core Asset. Institutional flows concentrate first and most in BTC, reinforcing its “digital macro asset” status.

- Second tier: ETH as the hub Asset. ETH serves as the nexus connecting Beta and application ecosystems, benefiting from institutional recognition of on-chain infrastructure.

- Third tier: Altcoins as high Beta. Altcoins remain nimble, but valuations will depend more on actual cash flow, user growth, and liquidity depth—pure narrative premiums will shrink.

This will upend the classic “altcoin-wide bull run.” The future is likely to feature “core assets in steady bull trends + thematic asset surges,” rather than broad-based market rallies.

Changing Pricing Mechanisms: Volatility as an Asset and Risk Premium Repricing

As yield-focused ETFs grow, volatility itself becomes a systematically priced asset.

Previously, markets focused on “Spot price moves.” Now, attention must also shift to “implied volatility surfaces,” “option seller supply,” and “term structure changes.” This drives two kinds of repricing:

- Risk premium repricing: risks that can be packaged into products see their premiums decline.

- Liquidity premium repricing: Assets with insufficient liquidity to absorb institutional flows may see discounts rise.

Institutionalization isn’t simply about “raising valuations”—it’s about “reordering valuations.”

Those included in standardized products and risk frameworks are more likely to attract long-term capital; those left in low-transparency, low-liquidity segments are at risk of marginalization.

Key Risks in the New Structure: Liquidity Mismatch and Overheated Narratives

Wall Street’s entry is structurally positive, but risks remain. Key risks to monitor:

- Liquidity mismatch: high liquidity in product shares doesn’t guarantee the same for underlying Assets during market stress.

- Concentration risk: excessive capital focus on a few core Assets may intensify “winner-takes-all” and drain weaker Assets.

- Derivative feedback risk: selling options in one-sided markets can trigger hedging flows, amplifying short-term volatility.

- Policy and compliance risk: regulatory shifts can directly impact product supply, distribution scope, and valuation frameworks.

Thus, market judgment requires more than asking “are institutions here?”—it’s critical to assess whether “institutional capital is sustainable, scalable, and resilient across cycles.”

How Investors Should Respond: A “Capital Structure First” Practical Framework

In this new cycle, shift your research focus from “price first” to “capital structure first.”

Use this checklist for weekly monitoring:

- Are Spot BTC ETF and yield ETF net inflows moving in sync?

- Are total Stablecoin supply and exchange Stablecoin reserves rising together?

- Is there a structural shift in BTC dominance or ETH/BTC strength?

- Is options market implied volatility diverging from Spot trends?

- Are altcoin rallies accompanied by deeper trading, not just sentiment-driven spikes?

For portfolio management, adopt a “core + satellite” framework:

- Core positions: focus on high-liquidity Assets for cross-cycle exposure

- Satellite positions: participate in thematic rotations, but with stricter TP/SL controls

- When capital indicators diverge, prioritize deleveraging over chasing late-stage gains

Ultimately, your Return ceiling isn’t set by how many hot trends you catch, but by whether you maintain discipline at inflection points in capital structure.

Conclusion

With Wall Street’s full-scale entry, the crypto market is moving from “narrative-driven” to “structure-driven.”

This is a long-term transformation in capital organization—not a short-term news event. Entry points are more traditional, products more complex, stratification deeper, and pricing more institutionalized. The future’s core competitive advantage is not just spotting opportunities, but understanding the capital logic behind them.

For investors, the most important step is to build a new consensus:

First, analyze capital structure—then price direction. First, manage drawdown—then pursue flexible Return.